Stay informed with free updates

Simply sign up to the German economy myFT Digest — delivered directly to your inbox.

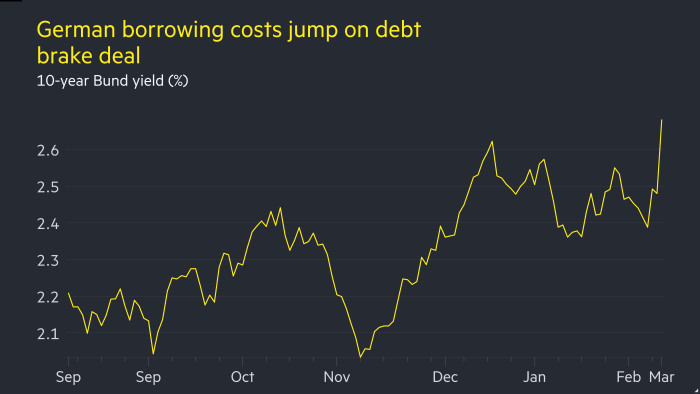

German borrowing costs surged by the most in 17 years on Wednesday, as investors bet on a big boost to the country’s ailing economy from a historic deal to fund investment in the military and infrastructure.

The yield on the 10-year Bund surged 0.21 percentage points to 2.69 per cent, its biggest one-day move since 2008, with markets braced for extra government borrowing.

Chancellor-in-waiting Friedrich Merz late on Tuesday agreed with the rival Social Democrats (SPD) to exempt defence spending above 1 per cent of GDP from Germany’s strict constitutional borrowing limit, set up a €500bn off-balance sheet vehicle for debt-funded infrastructure investment and loosen debt rules for states.

Deutsche Bank economists described the deal as “one of the most historic paradigm shifts in German postwar history”, adding that both the “speed at which this is happening and the magnitude of the prospective fiscal expansion is reminiscent of German reunification”.

Analysts at Goldman Sachs said the package could boost German economic growth to as much as 2 per cent next year — up from the bank’s current forecast of 0.8 per cent — if it is approved and implemented quickly.

The euro rose 0.7 per cent against the dollar to $1.069, its highest since November, and German stocks surged.

Merz is planning to push the changes through parliament this month before new lawmakers take their seats. Far-right and far-left parties won a blocking minority in the February 23 election and could prevent any constitutional change in the next legislative period.

The deal between Merz’s CDU/CSU group and the SPD still requires the support of the Green party to get to the two-thirds majority to change the constitution. The Greens have long called for reform to the so-called “debt brake” but senior party figures said that they first needed to digest the details of the plan. Analysts expect the party to ultimately acquiesce.

Cyrus de la Rubia, chief economist of Hamburg Commercial Bank, said the fiscal plan would quickly boost economic sentiment and growth as “companies and citizens will feel that something is finally being done”.

Economists had previously predicted continuing economic stagnation. Germany’s GDP has shrunk for two consecutive years as it grapples with high energy costs, weak corporate investment and feeble consumer demand.

“This fiscal sea change will permanently alter the way that Bunds are trading,” said Tomasz Wieladek, chief European economist at asset manager T Rowe Price.

Investors said the bond sell-off did not reflect concerns about the sustainability of Berlin’s debt, which at around 63 per cent of GDP is far lower than the level in other big western economies such as France, the UK and the US.

In contrast with recent rises in borrowing costs in countries such as the UK, which have threatened their fiscal plans, markets were pricing in a better growth trajectory that was boosting risky assets like stocks at the expense of ultra-safe government debt.

“Yields are rising because of the perception that Germany is turning on the growth tap. It is very risk-positive,” said Karen Ward, a strategist at JPMorgan Asset Management.

Germany’s Dax index, which had tumbled on Tuesday after the US imposed tariffs on some trading partners, surged 3.5 per cent.

German infrastructure companies were among the biggest gainers, with Heidelberg Materials up 14 per cent, while Siemens Energy rose 8.8 per cent. Thyssenkrupp, Germany’s largest steelmaker, gained 15 per cent.

Europe’s defence sector extended a blistering rally. Shares in Rheinmetall, Germany’s largest defence company, were up 4 per cent while Paris-listed Thales rose 6.7 per cent.

The gains spread to other European markets, with the continent-wide Stoxx Europe 600 up 1.4 per cent.

Asian stock markets earlier rebounded after comments from US commerce secretary Howard Lutnick that implied new tariffs on Mexico and Canada could be reduced.

Futures contracts tracking the US S&P 500 index were up 0.6 per cent. The dollar slipped 0.7 per cent against a basket of six currencies including the euro and pound.

Read the full article here