Algonquin Power & Utilities Corp. (NYSE:AQN) investors have witnessed the worst hammering despite some respite in early 2023. However, that early momentum was lost as sellers returned in May 2023. My caution in late March was timely, as I urged investors not to chase further upside, as it seemed priced in.

As such, while my earlier mean-reversion thesis worked out for a while, adding more positions by the end of March no longer looked attractive. My caution has panned out as AQN fell further toward its recent October 2023 lows. The interest rate monster reared its ugly head again as the 10Y yield surged to 4.89% recently, reaching a level not seen since 2007.

It also came nearly two months after Algonquin parted ways with its previous CEO, as it sought a new direction with the sale of its renewable energy business. As such, Algonquin attempts to channel its resources into becoming a pure-play regulated utilities business, as the current model is no longer sustainable.

Management stressed that Algonquin has scaled up, requiring more investments in its renewable energy business to keep up and deliver its targeted EPS growth range of between 5% and 8%. However, market conditions have shifted dramatically since the Fed started hiking rates rapidly in 2022.

As a result, I believe management’s decision is the right one, as the cost of capital would likely be unsustainable for Algonquin to deliver sustainable EPS growth while saddled with a heavy debt load (FY23 estimated adjusted EBITDA leverage ratio: 6.24x). It needs to provide confidence for investors in maintaining its investment grade rating, and taking on more debt to fund long-duration growth projects in the current environment could be highly perilous.

As such, Algonquin has taken the right steps here, although the timing seems off, as utilities stocks have been battered recently. Accordingly, Utilities Select Sector SPDR Fund ETF (XLU) has collapsed nearly 30% from its September 2022 highs through the lows this week.

As such, I believe Algonquin’s business transition plans could be under increased scrutiny, as the company could struggle to attain the valuations it hoped to achieve before the recent downward sector de-rating. As a result, it could delay its path to reducing leverage and improving earnings trajectory, potentially putting its remaining dividend payout under further stress of a cut.

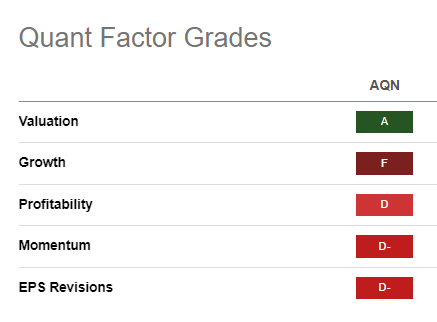

AQN Quant Grades (Seeking Alpha)

Seeking Alpha Quant assigned AQN an “A” valuation grade, corroborating the downward valuation de-rating. However, with weak factor grades underpinning its other vital metrics, investors must be cautious about potentially entering a value trap.

AQN price chart (weekly) (TradingView)

AQN’s price action suggests that dip buyers may have attempted to defend its October 2023 lows at the $5.40 level. It’s an incredulous, steep plunge for a stock on the precipice of entering penny stock status (<$5). Notably, AQN has collapsed nearly 70% from its 2021 highs, likely spooking income investors who believed multi-utilities are “safe” bets. However, Fed Chair Jerome Powell has other ideas, as the FOMC broke the multi-utilities growth story decisively.

The critical question underpinning a dip-buying opportunity facing investors is whether they believe a structurally sound recovery could occur from the current levels. If so, what could help drive it?

My conviction suggests that highly-indebted plays like AQN should be avoided. Coupled with the significant uncertainties on its business transformation, it could end up as a “dead money” stock for many years, potentially trapping value investors in a consolidation range, moving nowhere. While I anticipate a short-term rebound, I’m no longer optimistic about a more sustained upward recovery. Hence, unless you are a short-term investor adept at taking advantage of range-trading opportunities, an income investor should seek more attractive and higher-quality income opportunities.

AQN’s price action also suggests my previous mean-reversion thesis has been invalidated. As such, I urge investors to stay on the sidelines, and choose higher-quality plays that could withstand a higher-for-longer Fed.

Rating: Maintain Hold.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

Read the full article here