Thesis

The Calamos Dynamic Convertible and Income Fund (NASDAQ:CCD) is a convertibles securities CEF. The name is very interesting to cover and trade since it has a very high beta to the market, especially when the discount/premium to NAV structural feature is considered.

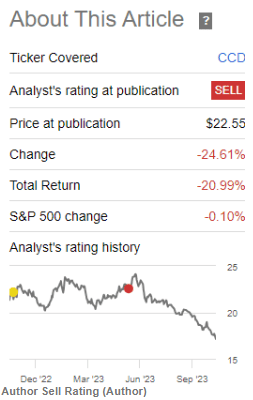

When we covered the name last year we wrote a piece called ‘CCD: Highest Premium In The Past Decade, Time To Sell’ back in May 2023. The CEF proceeded to lose over -20% next:

Rating 1 (Seeking Alpha)

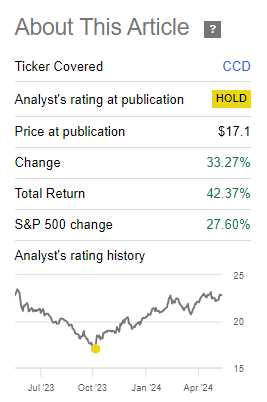

Our next article identified a bottom in the discount to NAV and our switch to Hold for the name. The article marked the bottom for the price in CCD, with the fund significantly up since:

Rating 2 (Seeking Alpha)

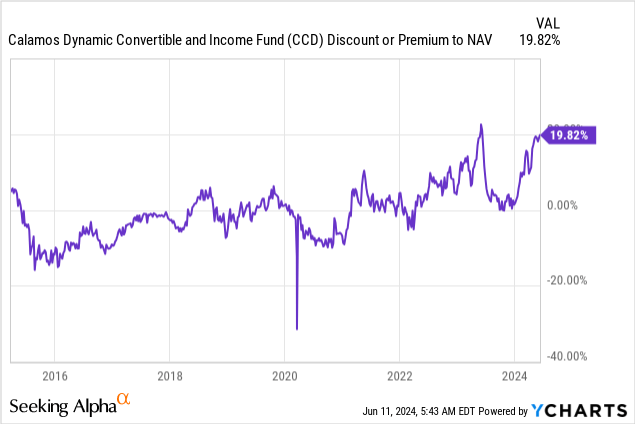

We are yet again looking at CCD since our systems have flagged a re-emergence of a historical premium to NAV, premium which we do not think will last.

In our current article we are going to analyze CCD in light of today’s macro environment, and highlight why we think the internals of the CEF are currently overbought.

High beta CEFs are meant for trading

There are certain CEFs which are high beta. High beta denotes names which are very volatile. Convertibles CEFs are generally more volatile than others because the underlying asset class consists of low yielding bonds with embedded options. CCD represents a pinnace in this instance, with its structural features also fluctuating greatly. We are talking here about the fund’s discount/premium to net asset value.

While some CEFs are ideal buy-and-hold names, high beta CEFs are meant for trading rather than just holding. As outlined in the ‘Thesis’ section above, following the signals provided by our articles could have netted returns in excess of 40% in the past year, returns which are not normal for regular buy and hold names. CCD is a fund that needs to be traded, and investors should have shorter than usual holding frames in mind in respect to this name.

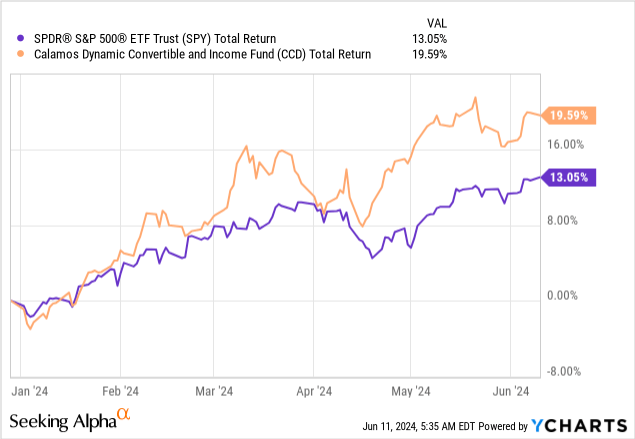

Equity markets have rallied

The wider equity markets have rallied significantly this year, especially on the large cap side:

CCD has been a high beta expression of that move, rallying over 19% in 2024. The fund contains low yielding bonds with convertible features, thus the embedded options have gained in value, especially for AI linked names:

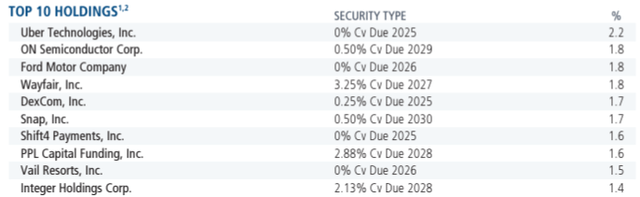

Top Holdings (Fund Fact Sheet)

The fund has a large technology sector bucket, allocation which has helped the name in 2024:

Sectors (Fund Fact Sheet)

Information Technology represents 25% of the fund, followed by Consumer Discretionary at 19.8% and Health Care at 15.9%.

Revisiting the highest premium to NAV in its history

With the market rallying and its underlying holdings moving up in price, the CEF is re-visiting its highest premium on record:

Our article last year highlighted the last top, namely when the premium to NAV was trading at 20%. The fund swiftly lost -20% during the next risk-off event. It will not be any different this time. Expect the current premium to NAV to move lower towards 0% during the next market sell-off.

This is what high beta CEFs do – they move up quite fast, but they equally sell-off violently. We do not think this time will be any different.

A retail investor simply needs to understand that structurally there is no reason for such a high premium to NAV, and as we can see from 2020/2021, the ‘regular’ premium to NAV for the name is somewhere around 1% to 5%.

Other CEFs have persistent premiums to NAV because they have cheap fixed rate funding (especially on the fixed income side), or the manager has an outstanding track record with very specific names. Neither of those factors are present here.

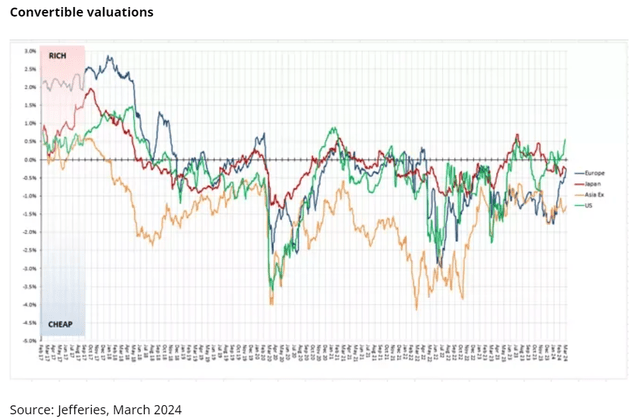

Valuations are again rich

Despite the low volatility levels as observed in the VIX, convertibles are again trading rich based on the stretched conditions in equities:

Valuations (Jefferies)

The above chart courtesy of Jefferies shows that US converts (green line in the above graph) have moved to ‘Rich’ territory. Convertibles are bonds with low coupons that have equity returns embedded in them via convertible features. If the underlying equity rallies, the bond is more valuable because the market prices it like an equity since the conversion is bound to happen. Equity performance (delta) is therefore the main driver here.

When convertibles do not convert

The CEF has a number of bonds with near term maturities, but stock valuations which are below the conversion price. Let us take Uber Technologies as an example. The fund holds the 0% 2025 bonds from Uber. You can find the prospectus for the bonds here on the SEC website. The conversion language on page 57 states:

Section 14.01. Conversion Privilege.

(A) Subject to and upon compliance with the provisions of this Article 14, each Holder of a Note shall have the right, at such Holder’s option, to convert all or any portion (if the portion to be converted is $1,000 principal amount or an integral multiple thereof) of such Note (i) subject to satisfaction of the conditions described in Section 14.01(b), at any time prior to the close of business on the Business Day immediately preceding September 15, 2025 under the circumstances and during the periods set forth in Section 14.01(b), and (ii) regardless of the conditions described in Section 14.01(b), on or after September 15, 2025 and prior to the close of business on the second Scheduled Trading Day immediately preceding the Maturity Date, in each case, at an initial conversion rate of 12.3701 shares of Common Stock (subject to adjustment as provided in this Article 14, the “Conversion Rate”) per $1,000 principal amount of Notes (subject to, and in accordance with, the settlement provisions of Section 14.02, the “Conversion Obligation”).

With UBER common shares currently at $68.6/share, the conversion rate yields an amount of only $848 (68.6 x 12.37). As it stands the bond holders are better off by receiving the redemption amount (i.e. the principal on the bonds) rather than convert into common shares.

Given the maturity of the bond is in 2025, equity prices for UBER common shares are the most important pricing element here. If they rally from here, the bonds will exhibit an almost 1:1 correlation with the common shares once they go significantly in the money.

Conversely, if the UBER shares continue to linger at the current levels, the bonds will price a regular return of principal, and thus trade at a discount since they offer a 0% coupon versus 5.3% on risk free treasuries. Given the close proximity of the maturity date, volatility will have less of an impact as time goes by, with the move in the common shares being the main driver.

Conclusion

CCD is a convertibles CEF. The fund has done very well in 2024, being up over 19%. The fund has a high beta to the overall market, and more importantly, exhibits a large beta for its premium to NAV. As the NAV moves up, the premium also increases. We are yet again close to a historic high in the premium to NAV for this CEF. The last time this event occurred was 2023, and the CEF proceeded to swiftly lose -20% and move to flat to NAV during the next risk-off event. We think this time will be no different. We are a sell here, penciling in a -15% down move during the next market sell-off.

Read the full article here