Investment thesis

A significant increase in shipments of Instinct MI300 AI accelerators and strong sales of EPYC processors drove data center revenue growth of 115% YoY and +21% QoQ in Q2 2024. Revenue from Instinct MI300 sales exceeded $1 billion for the first time in Q2 2024 and guidance for the full year 2024 was raised again, leading to a corresponding increase in our revenue guidance for the company.

AMD’s (NASDAQ:AMD) GPU revenue roadmap for 2024 was reaffirmed, which is positive for investor perception given the news of competitor NVIDIA Blackwell’s chip shipment delay.

Importantly, AMD’s revenue margin is improving faster than we expected (our previous article from June gave a HOLD rating and is accessible via this link), which has led to an increase in the EBITDA forecast.

Thus, we have raised our price target for AMD shares to $192 from $189. The rating is BUY.

Data Center segment growing faster

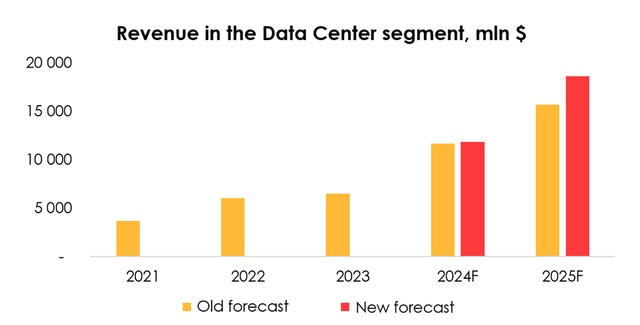

In 2Q 2024 AMD’s revenue in the Data Center segment rocketed to $2.8 bln (+115% y/y and +21% q/q), compared with our forecast of $2.6 bln, which was driven by robust growth in shipments of Instinct MI300 accelerators and strong sales of EPYC processors.

Speaking about EPYC, the company noted that major deals were concluded in 2Q 2024 across industry verticals: financial services, healthcare, commerce, transportation, technology including Adobe, Boeing, Industrial Light & Magic, Optiver, and Siemens. AMD also said it will provide these server processors for mission-critical workloads to companies such as Netflix and Uber. Importantly, over 1H 2024, more than 1/3 of server processor shipments to enterprise customers were to companies that were deploying EPYCs in their data centers for the first time. This means that, while meeting the growing demand from existing customers, AMD also successfully expands its customer base. The company expects that the fifth-generation of EPYC processors, the Turin, will be met with enthusiasm. Shipments to leading cloud customers already started in 2Q 2024.

As for the Instinct MI300 series, revenue from sales of these AI accelerators exceeded $1 bln in 2Q 2024 for the first time. The rising demand and, apparently, steady improvements in the supply chain allowed AMD to again raise its 2024 guidance for revenue in the GPU sub-segment, from $4 bln to $4.5 bln. The previously announced roadmap for this sub-segment, which runs to 2026, was reaffirmed. In light of the news about the delayed start of shipments of Blackwell chips by rival NVIDIA, AMD’s compliance with the previously announced schedule of new-product releases has a positive impact on the perception of the company by investors.

We are raising the forecast for revenue in AMD’s Data Center segment from $11.8 bln (+82% y/y) to $12.8 bln (+98% y/y) for 2024, and from $18.6 bln (+57% y/y) to $20.7 bln (+61% y/y) for 2025 as the company raised its guidance for revenue in the GPU subsegment, and also on the back of high demand for AMD equipment for data centers. We expect revenue in the Data Center segment to come to $3.59 bln in 3Q 2024.

Invest Heroes

The company’s other segments

Revenue in the Client segment totaled $1.49 bln (+49% y/y and +9% q/q), topping our forecast of $1.37 bln. Revenue growth was driven by strong demand for the previous-generation of Ryzen processors and the start of sales of the next-generation Zen 5.

We expect this segment’s positive revenue momentum to continue in the coming quarters, driven by a recovery in global PC shipments as well as ramped-up shipments of new Ryzen processors. Based on Phoronix independent tests, which used almost 400 different benchmarks, it was concluded that processors built on Zen 5 architecture show impressive results, and the architecture itself has a well-thought-out design. Much appreciation was given to the high performance and energy efficiency of processors built on this architecture. At the same time, prices for such models as Ryzen 5 9600X and Ryzen 7 9700X are lower than they are for basic similar models built on Zen 4, and more competitive compared with competition at Intel.

Given the segment’s strong results in 2Q 2024 and the good outcome of independent tests of the next generation of processors, we are raising estimated revenue in the Client segment over the forecast period to 2025. We expect 3Q 2024 revenue to reach $1.65 bln.

Revenue in the Gaming segment totaled $648 mln (-59% y/y and -30% q/q) in 2Q 2024, down from our forecast of $791 mln (which would have been a decrease of 50% y/y). Demand for consoles is not showing any signs of recovery:

- Sony PS5 sales declined in calendar 2Q 2024. According to the company, PS5 is entering the last phase of its life cycle. Sony again lowered its PS5 sales forecast for fiscal year 2025 (April 2024 to April 2025), from 21 mln units to 18 mln units (following last quarter’s cut from 25 mln units to 21 mln units).

- Xbox Series X/S sales are falling, with insiders asserting that Microsoft is going to wind down console sales in Europe, the Middle East and Africa on account that the Xbox Series X/S is losing competition to the PS5.

- Nintendo Switch sales also continued to fall, slumping by 46% y/y in calendar 2Q 2024. One of the reasons is the anticipation of news about the Switch 2 release, which, however, may not come until March 2025.

The only hope for a meaningful growth in sales of these consoles comes from the release of exclusive games, including the long-awaited release of GTA 6 in the fall of 2025 on PS5 and Xbox Series X.

We are maintaining a negative view on the Gaming segment’s revenue due to the ongoing trend for cross-platform games, which takes a toll on console sales, as well as the declining popularity of console games among younger generations, compared with the Millennials.

It is due to these reasons and the segment’s weaker 2Q 2024 results that we are lowering our expectations for the Gaming segment’s revenue over the forecast period to 2025. We expect it to reach $602 mln in 3Q 2024. Our forecast is in line with AMD’s expectation that sales in the Gaming segment will drop in 2H 2024 from the level of 1H 2024.

Revenue in the Embedded segment totaled $861 mln (-41% y/y and +2% q/q), which was close to our forecast of $871 mln. AMD said it is spotting the first signs of improvement in order patterns and expects revenue in this segment to gradually recover in 2H 2024. We expect the segment’s revenue to reach $887 mln in 3Q 2024.

Therefore, we are raising the forecast for revenue in the Data Center and Client segments in 2024 and 2025 and at the same time cutting the forecast for the Gaming segment’s revenue.

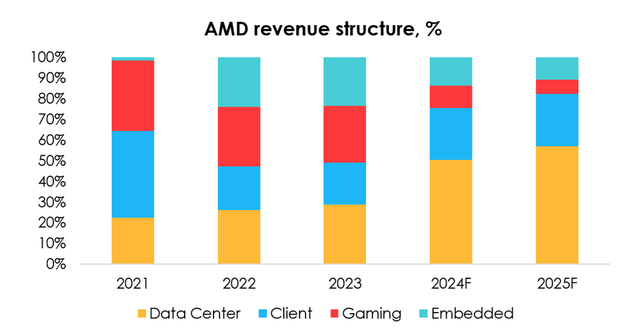

We expect that in 2024 the proportion of revenue from the Data Center segment in AMD’s total revenue will rise to 50% (+21 pp), and from the Client segment to 25% (+4 pp), given that the company’s key growth drivers continue to be in play in these two segments.

Invest Heroes

AMD’s financial results

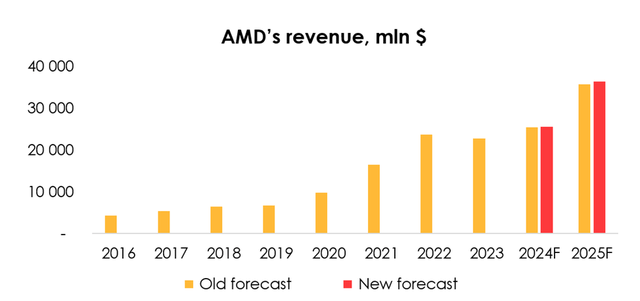

We are raising the forecast for AMD’s revenue from $25.3 bln (+12% y/y) to $25.5 bln (+12% y/y) for 2024, and from $35.7 bln (+41% y/y) to $36.3 bln (+42% y/y) for 2025, following the higher forecasts for revenue in the Data Center and Client segments, although that was partially offset by the lower forecast for the Gaming segment’s revenue.

Invest Heroes

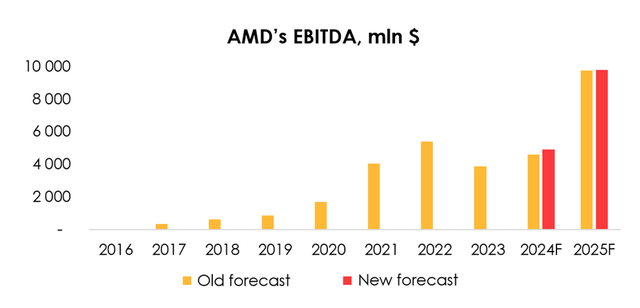

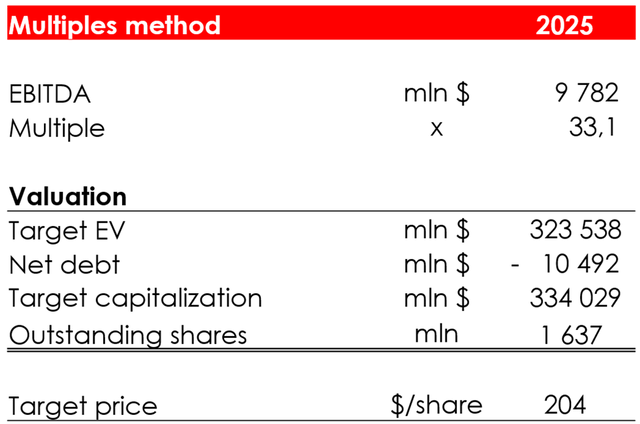

We are raising the EBITDA forecast from $4.58 bln (+19% y/y) to $4.9 bln (+27% y/y) for 2024, and from $9.74 bln (+113% y/y) to $9.78 mln (+100% y/y) for 2025 due to:

- the increased revenue forecasts for 2024 and 2025;

- the increase in the forecast for the company’s 2024 operating margin from 5.5% to 6.7%.

The increase in the forecast for the company’s 2024 operating margin is driven by the higher actual margin in 2Q 2024, which indicates some success in supply chain management for the MI300 and preparations for the start of MI325 sales. Despite the increase in the operating margin forecast for 2024, the outlook for 2025 remained unchanged at 18.7% as TSMC is expected to hike prices for chips that AMD uses in its products.

Invest Heroes

The outlook for the company’s free cash flow is that it will total $1.6 bln (+43% y/y) in 2024 and $6.75 bln (+321% y/y) in 2025.

M&A

First, AMD plans to close the deal to acquire the Finnish AI startup Silo AI for $665 mln in cash in 3Q 2024, which would be the largest such deal in Europe in the last 10 years (since Google’s purchase of UK-based DeepMind). Silo AI is Europe’s largest private AI lab with extensive experience in developing customized AI solutions for a variety of enterprise clients, including Allianz, Ericsson, Finnair, Korber, Nokia, Philips, T-Mobile and Unilever.

Second, AMD recently announced the acquisition of ZT Systems, one of the world’s leading providers of computing infrastructure. ZT Systems is a leading provider of server solutions. Based in New Jersey, ZT Systems has more than 15 years of experience designing and integrating data center infrastructure and storage systems for the world’s largest cloud companies. ZT Systems does not disclose the names of its customers, but it appears that in recent years it has expanded its profile by providing specialized support for some of the most complex and expensive aspects of designing an artificial intelligence computing architecture.

The total value of the transaction is $4.9 billion. The acquisition will be in cash and stock and is expected to close by mid-2025. Upon closing, ZT Systems’ computing infrastructure design business will become part of AMD’s Data Center Solutions business group, and the data center infrastructure manufacturing business will be divested. This transaction is another strategic step for AMD to strengthen its position in the data center AI equipment market and is positive news for the company.

We do not include the ZT Systems acquisition in the valuation due to the delayed closing and unclear financial outlook.

Valuation

We are raising the target price of the shares from $189 to $192 due to:

- the increased EBITDA forecasts for 2024 and 2025 (positive effect);

- the increase in the projected net debt from ($12.9) bln to ($10.5) bln (negative effect);

- the shift of the FTM valuation period, which makes future financial results closer by one quarter and reduces the discount factor (positive effect).

Based on the new assumptions, we are assigning a BUY rating to the stock.

The share price of $192 was achieved by computing the target price based on estimated financial results for 2025, and discounting it to the FTM price at the rate of 13% per annum.

The discount rate of 13% is the average growth of the S&P 500 Index over the past 20 years. In other words, when we value a company based on its long-term results, it is important to us that the company’s growth exceeds the average growth of the index.

Invest Heroes

Conclusion

AMD’s roadmap, which implies annual releases of a new AI accelerator, and the specifications of these accelerators hint at AMD’s serious determination to compete with NVIDIA. In order to ramp up production of the Instinct series, AMD still faces a lot of work to streamline the supply chain.

Read the full article here