By James Knightley, Chief International Economist

336,000 Job gains in September

Surging September jobs that no one saw coming

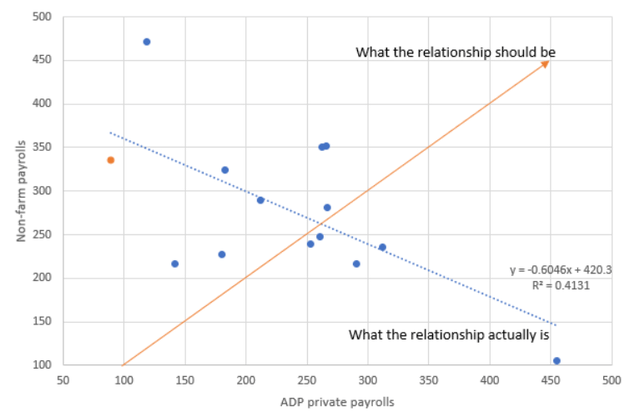

Well, what can you say when that happens? The US apparently added 336,000 jobs in September, while there were a net 119k of upward revisions to the past two months. The market had looked for 170k with a range of 90-250k amongst the banks and consultants who submitted forecasts. The ISM reports didn’t suggest anything like this would happen, nor did the NFIB employment numbers and neither did the ADP report, which showed an 89k increase. Well… actually it did in its own special way. The ADP is the best way of forecasting non-farm payrolls right now given its bizarre inverse relationship seen in the chart below. Based on the numbers since January 2022, 89,000 in ADP jobs pointed to 372,000 for payrolls, which would have been the closest forecast!

Inverse relationship between ADP payrolls and non-farm payrolls

Macrobond, ING

Broad strength with leisure and hospitality in the lead

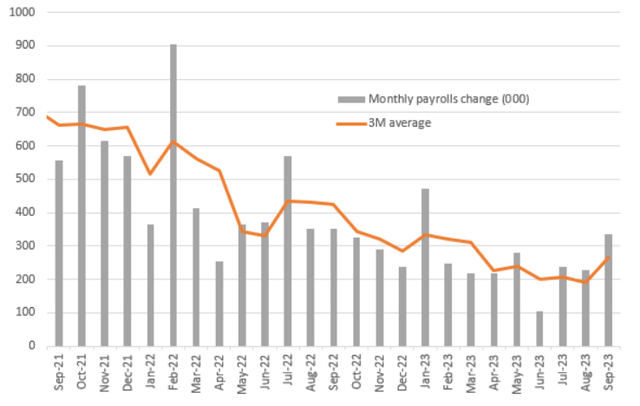

The details show private payrolls rising 263k, with government employment rising 73k. Within the private sector, leisure & hospitality increased 96k, with private education & health up 70k and trade and transport up 45k. This leaves the three-month moving average at 266k, which we can’t argue against given the strength we will likely see in 3Q GDP. We wouldn’t be surprised to see a 4% annualised expansion with Taylor Swift, Beyoncé and Barbenheimer helping to give growth a kick higher.

Non-farm payrolls monthly change & 3M moving average

Macrobond, ING

Some crumbs for the doves, but higher for longer remains the theme

Nonetheless, that is just the establishment survey of employers. The household survey used to calculate the unemployment rate was weaker, showing employment growth of just 86k, with unemployment rising 5k. This leaves the unemployment rate at 3.8% rather than dipping to 3.7%, which was what the market was expecting. Wages were more benign as well, rising 0.2% month-on-month or 4.2% year-on-year rather than coming in at 0.3%/4.3% as the consensus predicted.

There are always doubts about data quality when you get such wide discrepancies between different data sources, but payrolls is the number the market puts most emphasis on, and we have to acknowledge that such strength keeps alive the prospect of another rate rise and fits with the Fed’s higher for longer narrative surrounding the policy rate. The doves will cite the trending higher of unemployment and the subdued wage print, but that won’t matter much if next week’s CPI and PPI reports come in hot. The current consensus is for core CPI to rise 0.3% MoM, which is still too high for the Fed, which wants to see 0.1% or 0.2% MoM prints. We would still argue that monetary policy is restrictive enough and we don’t think that the Fed will hike again, but hot inflation will ensure we hit 5% on the US 10-year Treasury yield.

Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Original Post

Read the full article here