Co-authored with “Hidden Opportunities”

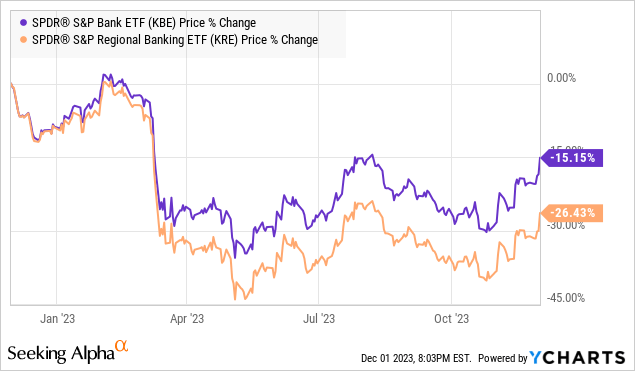

The failure of five banking institutions in the U.S. in 2023 rattled investors, and prominent regional bank stocks have sold off. Investors remain nervous about this market segment due to considerable doubts about these companies’ stability and risk posture.

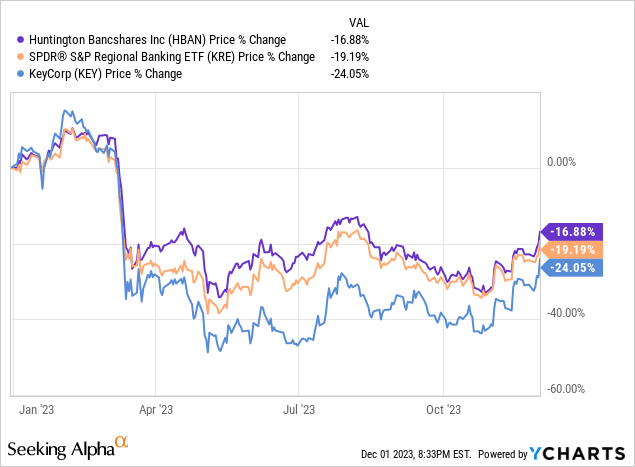

The SPDR S&P Bank ETF (KBE) and the SPDR S&P Regional Banking ETF (KRE) have sold off considerably, with the latter facing a much more significant impact from the financial sector fears.

Bill Gross is the co-founder and former chief investment officer of PIMCO (Pacific Investment Management Company), and during his legendary, multi-decade run, the company grew to manage trillions in net assets. The billionaire who is known for his expert techniques in navigating the bond and fixed-income markets through chaotic times, is reportedly buying Truist Financial Corp. (TFC), Citizens Financial Group (CFG), KeyCorp (KEY), and First Horizon Corp. (FHN).

Bill Gross believes the “regional bank falling knife has hit bottom,” suggesting that investing in regionals is no longer dangerous considering their deeply discounted valuation. We can see three main themes from the Q3 earnings reports of regional banks.

-

Modest growth in loan loss provisions and defaults

-

Interest income continues to grow, but net interest income is strained

-

There is modest growth in average deposits.

Loan loss provisions are not actual losses. The Financial Accounting Standards Board has adjusted the CECL (Current Expected Credit Losses) methodology to consider future forecasts, the current economic moment, and historical loss information. The reserve increase isn’t necessarily banks panicking over the future but an adjustment to a world where interest rates are not historically low anymore. Although late payments of 30 or even 90 days due have gone up, they are only off historical lows. We still see loan loss provisions and default rates below the pre-Covid levels. So whether it is the consumer side with auto and credit card loans or other loan categories, most of the banks and lenders are experiencing a slow return to long-term trends.

Bill Gross buying regional banks is not the only reason to load up. We see well-managed institutions have the bulk of their investment portfolio stashed in government-guaranteed instruments and maintain a high-quality loan portfolio with credit-worthy borrowers. These players maintain a robust balance sheet and are well-positioned to see substantial valuation improvement in the near term. But we like to get paid for our investment, and with current income being our prime focus, we seek the preferred securities of two well-run banks.

Let’s dive in!

Pick #1: HBAN Preferreds – Up To 7.1% Yields

Huntington Bancshares Inc. (HBAN) is the 26th largest bank in the United States, with $187 billion in assets under management. HBAN provides banking, payments, wealth, and risk management products and services to consumers, small and middle-market businesses, corporations, municipalities, and other organizations. HBAN operates over 1,000 branches in 11 U.S. states and maintains industry-leading scores in customer satisfaction.

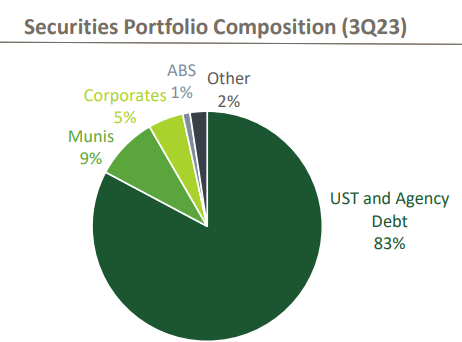

HBAN ended Q3 with more than 90% of its investment portfolio comprising safe and guaranteed asset classes – U.S. Treasures, agency debt, and municipal bonds. Source

Q3 Investor Presentation

Both consumer and commercial deposits saw modest growth during the quarter. The bank ended Q3 with a reported total liquidity of $91 billion as of September 2023, and its cash + borrowing capacity as a percentage of uninsured deposits was a peer-leading 204%. HBAN reported an industry-leading percentage of insured deposits, and its balance sheet carries A-/A3 ratings from leading credit ratings. HBAN’s Net Interest Income has seen an 8.7% CAGR since Q3 2021 and is up sequentially in comparison with Q2 2023 but down 2% YoY. As we approach the end of the rate hikes, prospects remain strong for continued NII improvement.

HBAN has been a reliable dividend steward, with common stock dividend growth in the past ten years. Its current quarterly payment calculates to a 5.3% annualized yield and comes at a modest 42% payout ratio.

HBAN’s CRE (Commercial Real Estate) portfolio stood at 10% of total loans, well below the peer average, with higher exposure to multi-family homes. Even in the risky auto loan segment, HBAN had its customer average FICO score at 778 and Net Charge Offs well below the peer average.

We like HBAN common stock but find its deeply discounted preferreds to be particularly attractive in the current market conditions. These are BB+ rated and pay Qualified Dividends to shareholders.

-

4.50% Series H, Fixed-rate, Non-Cumulative Perpetual Preferred (HBANP), yield 6.2%

-

5.70% Series I, Fixed-rate, Non-Cumulative Perpetual Preferred (HBANM), 7.1%

-

6.875% Series J, Rate-reset, Non-Cumulative Perpetual Preferred (HBANL), yield 7.0%

HBANM yields 7.1% and offers 28% capital upside to par value. This preferred will pay this high fixed interest rate until redemption.

If you prefer floating-rate exposure, the newly issued HBANL offers a 7% yield. If unredeemed after its April 2028 call date, this security’s coupon will float at 5-Year T-bill + 2.704%, which will reset every five years.

Pick #2: KEY Preferreds – Up To 7.5% Yields

KeyCorp (KEY) has 190 years of operating history and is the 16th largest banking institution in the U.S., with $198 billion in assets under management. KEY offers deposit, lending, cash management, and investment services to individuals and businesses in 15 states.

During Q3, KEY reported modest growth in both consumer and commercial deposits. Two-thirds of KEY’s deposits are insured or are collateralized. Within the loan segment, 16% of KEY’s portfolio is Commercial Real Estate with greater allocation to multi-family homes. The total exposure to office loans is a sector-leading 0.7%. KEY places a strong emphasis on the creditworthiness of its borrowers, with a Weighted Average FICO score at origination of 768. The bank maintains adequate liquidity and is well-capitalized, and its senior long-term debt carries an A- rating by Fitch.

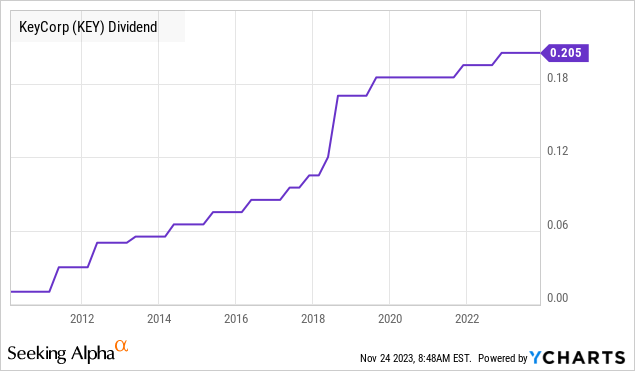

KEY common stock has seen growing annual dividend payments since 2010, and its current yield stands at 6.2% at a 66% payout ratio.

KEY has four classes of publicly traded preferred securities that pay Qualified Dividends and trade at deep bargain levels.

-

6.125% Fixed-to-Float Perpetual Non-Cumulative Preferred Stock Series E (KEY.PR.I), yield 6.9%

-

5.650% Fixed Perpetual Non-Cumulative Preferred Stock Series F (KEY.PR.J), yield 7.1%

-

5.625% Fixed Perpetual Non-Cumulative Preferred Stock Series G (KEY.PR.K), yield 7.0%

-

6.200% Fixed-to-Float Perpetual Non-Cumulative Preferred Stock Series H (KEY.PR.L), yield 7.5%

BB+ rated KEY-K presents a 7% yield and a 24% capital upside to par value, making it a solid bargain for fixed-income seekers. For those seeking floating rate exposure, KEY-L offers an 7.5% yield and a 20% upside to par. This security experiences a coupon reset with a high base coupon – 5-Year Treasury Bill + 3.132% if unredeemed after its call date in December 2027. The reset rate is locked for five years.

Conclusion

We are bargain hunters but seek attractive waiting fees to make the investment worth our while. We are building a rate-agnostic portfolio, and our preferred and baby bond portfolio has +45 securities with an overall yield of +9%. We see very attractive discounts in the regional bank sector but are treading softly (no pun intended) with our selections.

This regional bank sell-off presents a rare opportunity to lock in sizable yields for the foreseeable future. We see HBAN and KEY experience sharp sell-offs along with the broader sector despite strong operating fundamentals to thrive past the near-term uncertainties.

It will take time for confidence to return in the sector, but preferred dividends are an immediate cash collection with a higher degree of safety; we get paid to wait for the markets to realize the potential of these companies. Both Huntington Bank and KeyCorp are run by experienced management teams and have been good dividend stewards for years. These banks are attractively priced by book value metrics and have well-supported common stock dividends. We are locking in the +7% qualified yields from their deeply discounted preferreds.

Read the full article here