For us, Joby (NYSE:JOBY) belongs to a unique category of stocks that we refer to as “Project Stocks.” We believe these types of stocks are more like publicly traded VC shares vs traditional publicly traded businesses as they typically have $0 revenue and are closely tied to the development of an industry. Currently, Joby Aviation has no revenues or earnings and the entire upside of JOBY lies in the successful design, development, production and operation of their eVTOL aircraft. Currently they have a functioning and flying test bed and are working with their strategic manufacturing partner (and largest external shareholder) Toyota (TM) on the development of their production lines. However, the lack of current market orders and the cash burn limits us to the rating of ‘Hold’ with a price target of $7. We believe that while this is a promising business, the current valuations suggest it might be better to wait for a more favorable entry price or adopt a strategy that minimizes costs. We plan to take advantage of elevated volatility levels in the stock and sell short-dated ITM call options and using the proceeds to purchase Joby’s Warrants (NYSE:JOBY.WS) which will give us long term leverage upside. We believe this trade presents a better Risk/Reward relationship relative to just owning shares at current prices. Further details of this trade are at the end of this article.

Overview

The dream of eVTOL (electric Vertical Take-Off and Landing) encapsulates a vision of the future where urban skies are punctuated with quiet, clean, and efficient electric aircraft, seamlessly transporting people and goods across cities and metro areas. Beyond the allure of futuristic skylines, this dream signifies the aspiration to overcome modern urban challenges—congested roads, lengthy commutes, and pollution—by leveraging cutting-edge technology. The promise of eVTOL envisions a world where urban residents can save time, diminish their carbon footprint, and relish unparalleled mobility, reshaping cityscapes and altering how we engage with our cities. These aircraft are designed to carry payloads of up to 1,000 pounds and are anticipated to be used for trips spanning up to 100 miles.

The key to their valuation is going to be meeting or exceeding their development timeline while maintaining spending targets and limiting equity dilution. Regulatory hurdles can be a massive roadblock for burgeoning industries but especially so for aviation companies. Currently, Joby has been receiving support from political figures, including California Governor Gavin Newsom and representatives from President Biden’s Advanced Air Mobility Interagency Working Group, further solidifying its position in the industry and providing much needed governmental and regulatory support towards the development of the aircraft and the overall eVTOL industry.

Initially planned for the 2030s, the FAA has moved the timeline for the publication of their regulations concerning eVTOL commercial operations forward to 2028, a move linked to the timeline of the LA Olympics that year. This timeline shift works favorably for Joby and it ideally will help them get through FAA certifications and into commercial operations faster as there will be much more clarity concerning requirements and the market that eVTOLs can support. The company plans to commence commercial operations in 2025. Given their current financial status, advancements in aircraft development, and the FAA SFAR documentation from 2024, they believe they are in a strong position to meet this target.

Additional aircraft are scheduled for delivery to Edwards AFB, which, combined with the initial delivery, will provide the company with the opportunity to test and refine its products in a real-world setting. As part of the contract with the DoD, numerous Air Force pilots have already completed Joby’s pilot training program, which includes simulator training and remote piloted flights. This training has been designed to ensure the smooth operation of the aircraft and to facilitate seamless integration into the existing structures at Edwards. Flight testing at Edwards provides the DoD with real exposure to these new aircraft and allows them to test their various capabilities. Air mobility, especially across the Pacific, is becoming a major focus for the DoD and the testing of JOBY’s and Archer’s (ACHR) aircraft may present opportunities at a tactical level for the military. We see the chances of large scale orders for eVTOL aircraft to be low in the near term (1-3 years) but the chances of a large contract win in the future are non-zero.

Quarter Review

Joby Aircraft has had an impressive second quarter in 2023, successfully achieving all of their prior stated goals for the first half of the year. This includes the significant accomplishment of rolling out their first production prototype, extensive ground testing, and the aircraft’s inaugural flight. All of which mark a significant milestone in the company’s growth trajectory. This production prototype confirms manufacturing and design processes, and while still subject to change, is likely 95%+ of the final design.

While progress is being made in various aspects, the selection of a site for their scaled manufacturing facility is taking longer than expected. This delay is attributed to the high level of interest in hosting the facility, which is a promising sign of the company’s perceived value and potential. Likely various communities, cities and states are offering varying incentives. The lack of a location for their major manufacturing site raises questions concerning the timeline of widespread commercial operations due to the limited capacity of their current manufacturing pilot line.

Toyota Links

Joby’s strategic partnerships have also contributed to their progress this year. Toyota has been an invaluable partner in helping ramping up manufacturing. In fact, Ted Ogawa, President and CEO of Toyota North America, joined Joby’s Board of Directors on July 1. This partnership is backed up by Toyota owning 11% of all outstanding shares and they are also the exclusive parts suppliers for all Joby aircraft. We believe this partnership is extremely beneficial, manufacturing is incredibly difficult especially at scale. Toyota invented and perfected many of the tools and processes that global manufacturing uses today. The structure of this partnership we believe is extremely powerful. Toyota has an incredibly diverse manufacturing background and should easily handle many of the requirements for JOBY while simultaneously providing valuable insight into JOBY’s own production lines.

Equity Issuance

As seen with SPCE, ASTR, GOEV, FSR and the multitude of other ‘Project Stocks’ we see equity raises being used to fund development and shore up cash balances. Companies with no revenue face significant challenges when trying to raise corporate debt due to their limited ability to repay those debts. Raising funds from equity can be a strong strategic move when shares are trading significantly higher than revenue and earnings can support but this is always going to be a risk factor for common equity holders. These projects are often industry defining and are extremely expensive. JOBY is no exception, during the latest quarter basic share count outstanding jumped from 631 million in Q1 2023 to 693 million shares at the end of the Q2 2023. A QoQ increase of 8.9% and a YoY increase of 14.3%. Paul Sciarra, Joby’s Executive Chairman, pointed in the latest earnings call that these recent capital raises have allowed the company to accelerate and invest in the pilot production line. This large increase in share count came from Baillie Gifford and SK Telecom, amounting to $180 million and $100 million respectively, received in May and June. Taking the $280 million in proceeds and dividing it by the 62 million share increase we get a rough price per share issued of $4.50. With shares currently trading at $7.50, waiting on the raise would have been massively beneficial.

While the effect of this issuance is not felt significantly because of the rise in share price of 37% over the course of the year it is a hidden weight on the stock and we see dilution risk continuing and even increasing as the share price climbs.

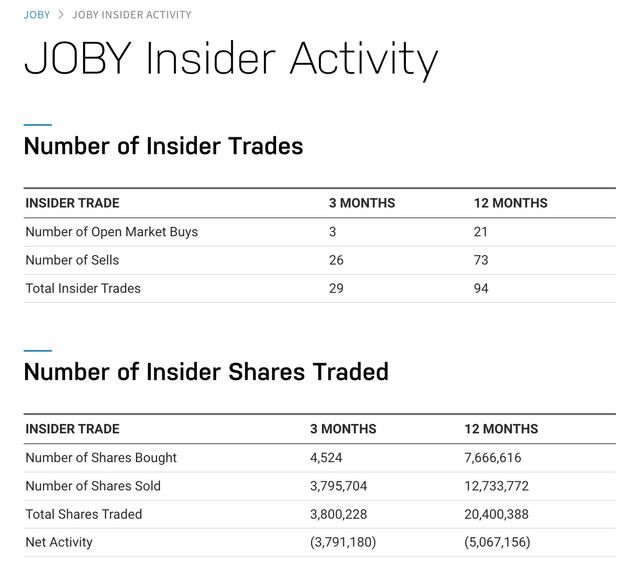

Insider Activity

Nasdaq

This issuance of stock comes on top of rather dramatic insider selling. These sales are cause for limited concern as the timing for a majority of the sales came shortly after the announcement of successful flight tests. We believe this was insiders taking advantage of a significant pricing catalyst and made a logical decision to sell. While not ideal from an equity stand point we believe this is a “wash” for rating aspects.

Balance Sheet

With no revenue in the near term, the valuation and equity returns of JOBY must come from the strength of their balance sheet and their chances of survival while also getting their product to market. After the latest equity sales Joby’s balance sheet is actually improved since the end of Q4 2022. Cash and Short Term Assets has climbed from $1.057 Billion to $1.195 Billion over those two quarters despite no earnings and high spending. With interest rates remaining elevated this sizable amount of cash should generate more of a fair amount of interest yearly. If we assume an average interest rate of 4% this would generate ~$48 million. With management maintaining their spending guidance for the full year, forecasting expenditures between $360 million to $380 million this $48 million actually reduces burn by 13%. If we assume that the burn rate remains elevated the current runway would be ~3.25 years which puts their runway to 2027 or just short of the 2028 Olympics. Unless we see high margin production and operation in the next 2-3 years we believe we are very likely to see further equity dilution. The one caveat is with so many shares outstanding already is that the % impact of further dilution is actually reduced and any increase in share value will also minimize the amount of shares that need to be sold to generate the same amount of cash.

Relative Valuation

Currently the Enterprise Value of Joby sits at $3.5 Billion while the Enterprise Value of their direct competitor ACHR, sits at $1.5 Billion. This values Joby at ~2.3x ACHR. As things sit currently JOBY has a slight lead from a development timeline perspective with ground tests and flights of their production-prototype. ACHR isn’t far behind and anticipates to have first flights this summer and with summer quickly coming to a close we imagine that first flight is also around the corner. Both companies have significant cash burn but ACHR has recently been award a large DoD contract of $142 million for 6 aircraft. This contact is given on the tail end of the $55 million contract extension given to Joby which brought that contract up to $132 million for 9 aircraft. While we cannot see what other services are included in these contracts, we can assume both contracts factor in similar levels of pilot training and infrastructure. So we believe that we can compare these two contracts to begin to get a picture of each company. Assuming that both JOBY and ACHR breakeven on these contracts JOBY is much more competitive with a per aircraft cost of $14.7 Million vs $23.7 million per aircraft for ACHR. We believe, while not a perfect comparison, it is a good example of the operational advantages that JOBY has over ACHR. This advantage likely comes from their partnership with Toyota and this comparative advantage is only likely to expand if production ticks up dramatically. We believe that JOBY will be able to scale much more efficiently than ACHR all else being equal.

Risks

We believe the risks are evident for JOBY. If the company cannot generate significant profit before cash runs out, there’s a solid chance of bankruptcy or more likely equity dilution. If the FAA delays the publication of their regulations this will push out Joby’s operational timeline and will negatively impact their first mover advantage and their time to market. The upside risk is likely to come from production news, contract news, or further aircraft development in either Joby or Archer.

Conclusion

Joby is well-positioned to benefit from sector tailwinds in the eVTOL space and we believe their premium over ACHR is justified. They are well capitalized to reach their anticipated commercial launch in 2025 but they will likely need to raise more cash to fund their larger ambitious goals. We believe this extra cash is likely to come from equity raises. In the near term, they have a hint of operational advantage over their competitors and the Edwards AFB real life applications are going to benefit product development, testing and pricing. The exposure to the DoD presents significant upside if a massive defense contract is ever pursued. The dilution risk and cash burn are very serious risks however. We believe that until a lot of the market dynamics are locked in that we cannot give this stock a ‘Buy’ rating and must give it a ‘Hold’ rating with a price target of $7.

We believe that holding JOBY at current prices offers limited upside in the 0-1 year time frame but we do believe that there is opportunity longer term. If we assume Enterprise Value stays near the current $3 Billion valuation, the short term cash burn is going to erode Market cap all else being equal. We believe in order for the business to trade at elevated levels we need to see profitable production and services which isn’t likely to be significantly seen until 2025 at the earliest.

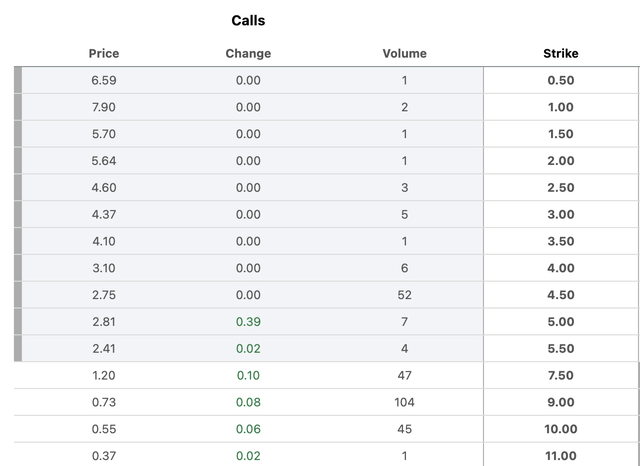

We plan to initiate the following trade. With shares currently trading at roughly $7.50 and the $11.50 warrants trading at $1.60 and Jan. ’24 call options currently trade based on the following chart.

Seeking Alpha

We plan to initiate a covered call while simultaneously purchasing the warrants. We will be purchasing shares and selling ITM or ATM calls and using the cash generated to purchase the warrants.

This will leave us exposed to any significant price decreases but we believe the chances of extended declines below $4-$5.50 are unlikely considering the list of catalysts we described above.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here