Microsoft (NASDAQ:MSFT) (NEOE:MSFT:CA) is scheduled to report its Q4 earnings on July 30th after the market closes. I presented my ‘Strong Buy’ thesis in my previous article published in April 2024, pointing out that Copilot and Azure AI could potentially extend Microsoft’s existing technology advantage. In Q4, I anticipate a strong growth in its intelligent cloud business. I reiterate my ‘Strong Buy’ rating with a one-year target price of $530 per share.

Expect Strong Growth in Cloud Business

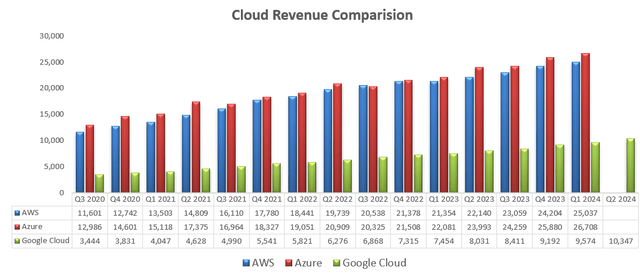

Alphabet (GOOGL) reported its Q2 result on July 23rd, reporting a 28.8% year-on-year in cloud revenue, making its cloud business a significant growth driver for Alphabet. During Alphabet’s earnings call, their management expressed strong confidence in its cloud business growth in the near future, driven by strong AI workloads and the digitization transformations from enterprise customers.

As depicted in the chart below, Microsoft’s Azure has been growing significantly over the past few years, leading the competition among the major hyperscalers.

Microsoft, Amazon, Alphabet Quarterly Earnings

I anticipate Microsoft’s cloud business will grow by 20%+ in the coming quarter for the following reasons:

- During the last earnings call, Microsoft’s management disclosed that the company had been experiencing more large deals for its Azure business, as enterprise customers accelerated its digitalization journey to execute AI training and inference workloads. I think these large deals could fuel Azure’s growth in the coming quarters.

- The strong growth in Google Cloud proves that AI workloads are stimulating the demand for cloud infrastructure and computing. With the rising popularity of AI, I forecast Azure and Microsoft’s other cloud platforms will benefit from the megatrend.

- As discussed in my previous articles, Microsoft possesses strong technology advantages for its cloud platform, as the company provides comprehensive software/operating system solutions to enterprise customers. The integrated solutions could give the company unique advantage over its competitors.

Global IT Outrage

On July 18th, CrowdStrike (CRWD) released an update that began to cause a global IT outrage. Although it is not Microsoft’s fault, the incident has affected 8.5 million PCs globally. In addition, it shows that Microsoft has the risk of allowing third-y to access its core kernel system. I anticipate the incident will lead to numerous lawsuits in the near future, especially from airlines and other enterprise customers. However, these lawsuits should be filed against CrowdStrike.

I anticipate Microsoft will update its internal R&D control policies related to third-party software vendors, and their management should address this issue during their Q4 earnings call.

Growth Outlook and Valuation

I break down Microsoft’s growth as follows:

- Intelligent Cloud: as discussed previously, I anticipate its Intelligent Cloud continues to grow at 20%+ in the near future, and the key growth drivers are AI workloads, digitalization and cloud adoptions.

- Productivity and Business Processes: I anticipate the segment will be driven by Office 365 adoption and ARPU growth through E5. I anticipate Office 365 to grow at mid-teens, and the Productivity and Business Processes segment will grow at 12% annually.

- More Personal Computing: The segment growth rate will be aligned with the PC volume growth and some growth from pricing. AI PCs could be a long-term catalyst for Windows operating systems when most enterprise customers begin to prepare AI inference workloads. The global PC market has been growing at 3%-4% in the past, and I anticipate More Personal Computing will grow at 6% annually, assuming 4% volume growth and 2% pricing growth.

As such, I anticipate Microsoft will grow its revenue by 14% organically in the near future. In addition, I assume the company will invest 6% of total revenue in acquisitions, contributing 1% to the overall topline growth.

In recent years, Microsoft’s management has been managing its cost structure to expand its operating margin. I model 30bps annual margin expansion driven by: 10bps expansion from gross profits; 10bps leverage from R&D and 10bps leverage from SG&A.

The DCF summary is:

Microsoft DCF – Author’s Calculations

I calculate its free cash flow from equity (FCFE) as follows:

Microsoft DCF – Author’s Calculations

The cost of equity is calculated to be 12% assuming: risk free rate 4.2% (US 10Y Treasury Yield); beta 1.12 (SA); equity risk premium 7%. Discounting all the future FCFE, the one-year price target is estimated to be $530 per share.

Key Risks

As communicated over the last earnings call, Microsoft expects its capital expenditure to increase materially on a sequential basis, driven by cloud and AI infrastructure investments. While I view these spending as necessary investments, the high capex spending could put some growth pressure on its free cash flow in the coming years.

For the on-premises business, I anticipate Microsoft will continue to experience growth pressures as more enterprise customers are moving their workflows to cloud. However, these businesses are very small compared to Microsoft’s cloud business; therefore, the growth impact is minimal.

End Notes

I anticipate Microsoft will continue to deliver 20%+ growth in its cloud business in the near future. Microsoft is well positioned in the AI era to capture growth from both infrastructure and AI platforms. I reiterate my ‘Strong Buy’ rating with a one-year target price of $530 per share.

Read the full article here