Shopify (NYSE:SHOP) stock has seen sideways momentum for the last few weeks despite posting good results in the recent quarter. One of the reasons is the bull run in early 2023 due to which the stock has seen over 60% jump in year-to-date. Shopify has been able to reignite revenue growth in the last few quarters and there are strong tailwinds that can help the company improve its topline. At the same time, Shopify has been able to improve the conversion of Gross Merchandise Value or GMV into revenue due to better services. Shopify’s GMV has increased 11x between the last quarter of 2016 and the last quarter of 2022. During this time, Shopify’s quarterly revenue base has increased from $130 million to $1.7 billion or 13x.

Shopify’s GMV for 2022 was $195 billion and rapid growth in this key metric should help the company improve monetization. The company has also undertaken some cost-cutting which is having a positive impact on the bottom line. Analysts have forecasted Shopify’s EPS at $1 for fiscal 2025 which means that the stock is trading 60 times the EPS estimate of 2025. However, better monetization and focus on cost optimization could help the company deliver good EPS growth in the next few quarters. The PS ratio is also at 12 which is significantly lower than the pre-pandemic years. Shopify stock can deliver good returns in the long term as the company adds new services and improves its GMV growth trajectory.

Better top-line growth

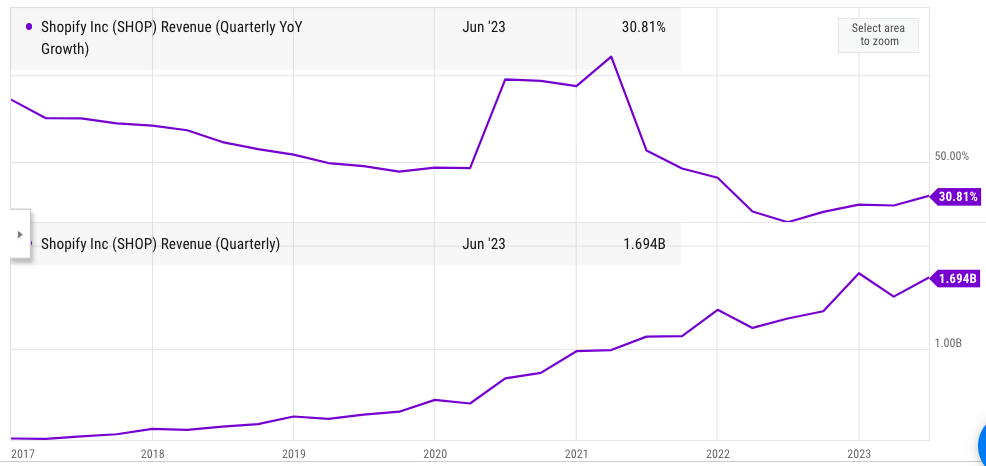

Shopify reported a GMV of $5.5 billion in December 2016 quarter. This has increased to $60 billion in the recent December 2022 quarter. Hence, Shopify’s GMV has increased to 11 times within the last seven years. On the other hand, Shopify’s revenue during the December quarter has increased by 13 times, from $130 million to $1.7 billion. This growth trend shows that the company is able to convert more GMV into actual revenue. One of the main reasons behind this trend is that Shopify is adding new services and it can charge customers a higher commission for these services.

Ycharts

Figure: Quarterly YoY revenue growth and revenue base of Shopify in the last few years.

Shopify’s GMV for 2022 was a staggering $195 billion. The company has been able to reignite revenue growth in the last few quarters. The YoY revenue growth hit a bottom of 15% in June 2022. Since then the YoY revenue growth has picked up again as the company faces easier comps. In the recent quarter, the company reported YoY revenue growth of over 30% which is quite high when we consider that the GMV base of Shopify is more than $200 billion.

Higher profitability trajectory

The revenue growth will not build a bullish momentum for the stock unless the company can deliver sustainable profitability. During the pandemic years, Shopify’s revenue growth and high EPS helped the stock reach its peak. The company would need to focus on profitability in the next few quarters in order to rebuild a long-term bullish rally. Shopify has divested from its logistics business which should help improve the bottom line. We should also see better monetization of current services as the company tries to build new AI tools.

Ycharts

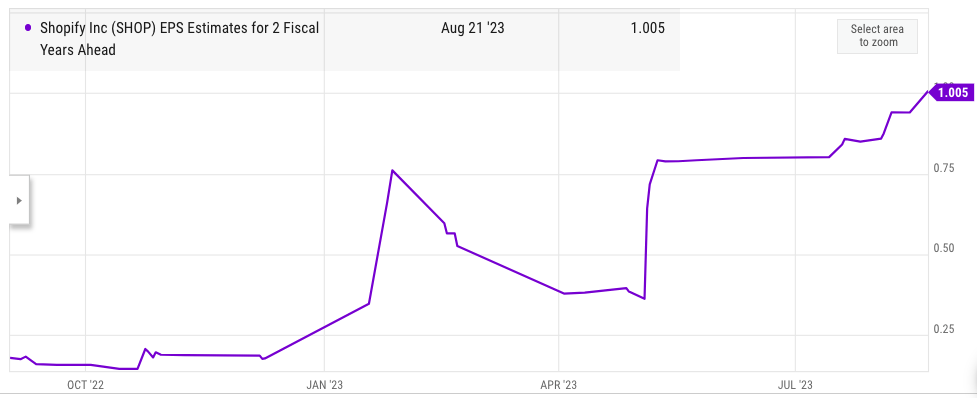

Figure: Increase in forward EPS estimates.

The EPS estimates for 2 fiscal years ahead have steadily improved in the last few quarters. According to current consensus, Shopify should be able to deliver EPS of $1 in fiscal year 2025. However, it is highly likely that Shopify will beat these estimates as the company launches new initiatives to improve monetization of its massive GMV base. Shopify’s trailing twelve months EPS during the peak of the pandemic went to $2.6. If the company can get close to this EPS rate by 2025, we should see a significant bullish run in the stock. The recent cost-cutting should also help the company improve the bottom line. We have seen a similar trend in all the Big Tech companies who have reported a rapid growth in EPS as their headcount was reduced.

Pricey valuation

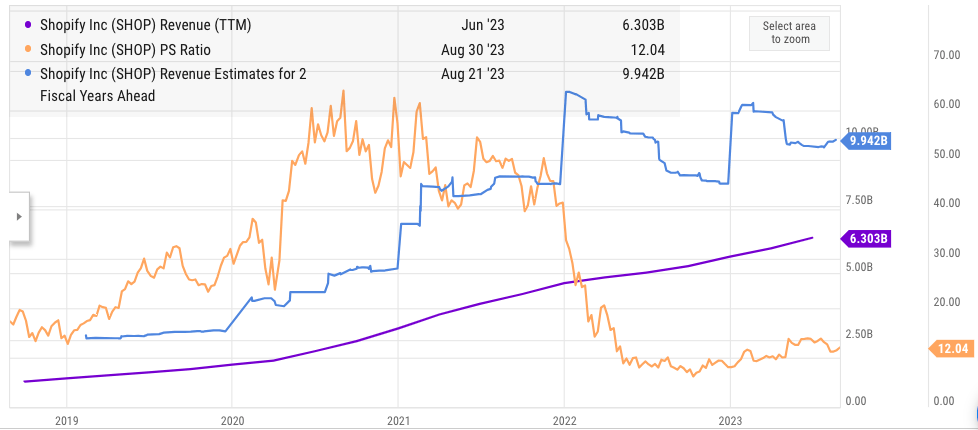

While most analysts agree over the long-term revenue growth potential of Shopify, some of them are wary of the pricey valuation of the stock. Shopify is trading at 12 times its PS ratio. This is quite high when we compare with most of the other tech players and even Shopify’s peer like Wix (WIX), Etsy (ETSY), and others. However, it should be noted that Shopify’s PS ratio is significantly lower than the average PS multiple prior to the pandemic when the stock had an average PS ratio of over 20.

Ycharts

Figure: Shopify’s PS ratio and revenue metrics.

Shopify’s revenue estimates for 2 fiscal years ahead is close to $10 billion which is equal to annualized revenue growth of over 25%. If we look at this metric, Shopify stock is trading at 7 times the revenue estimate of fiscal year 2025. This looks reasonable if the company can also manage to improve its EPS trend over the next few years.

The long-term tailwind from ecommerce growth is still very strong. Shopify will benefit from an increase in GMV and a higher ecommerce market share in key markets. This should help the company gain pricing leverage over other competitors and also improve its monetization momentum.

Investor Takeaway

Shopify has reported a faster revenue growth rate compared to its GMV growth in the last few years. This shows that the company is able to charge higher rate for additional services. There has been an acceleration in revenue growth over the last few quarters. Shopify has also divested from logistics services which were pulling down the profitability of the company.

Shopify could deliver over 20% YoY revenue growth for the next few years as the company gains from strong tailwinds within the ecommerce business. If Shopify regains its earlier ttm EPS of $2 by 2025, we could see a strong bull run within the stock. While the stock is not cheap, it seems to be reasonably valued and longer-term investors could gain a better return from Shopify, making the stock a Buy at current price.

Read the full article here