No matter the positive growth story from SoFi Technologies (NASDAQ:SOFI), the stock just limps along. The market is fixated with GAAP profits, yet the company is already highly profitable, warranting a higher stock price. My investment thesis is ultra Bullish on the stock based on the big 2026 financial targets and the lagging stock price disconnected by investors due to constant irrational fears.

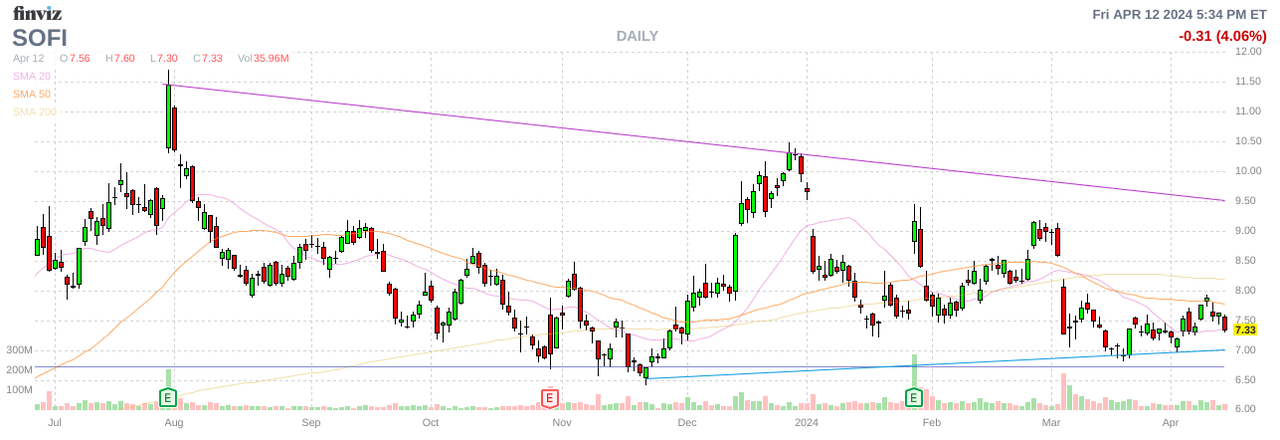

Source: Finviz

Always Negative Spin

SoFi recently completed a convertible debt offering for $750 million that tanked the stock. The stock market immediately viewed the debt offering as a negative, with a view the fintech needed to raise cash due to the recent lack of selling loans.

CEO Anthony Noto did a tour to discuss the offering and clearly highlighted how the 1.25% convertible debt with interest payable semi-annually in arrears and maturing on March 15, 2029 replaced existing preferred shares costing 12.5% with the debt jumping to a 15.0% rate in May for 5 years, if not repaid. The debt offering was a necessary and smart move to save $40 to $60 million in interest expenses, with SoFi forecasting the transaction being accretive to tangible book value.

Regardless, the stock hasn’t recovered and ended last week trading down at only $7.33 after topping $9 following earnings. SoFi reported strong growth during 2023 despite headwinds in the lending market and the market has mostly yawned.

2026 Targets

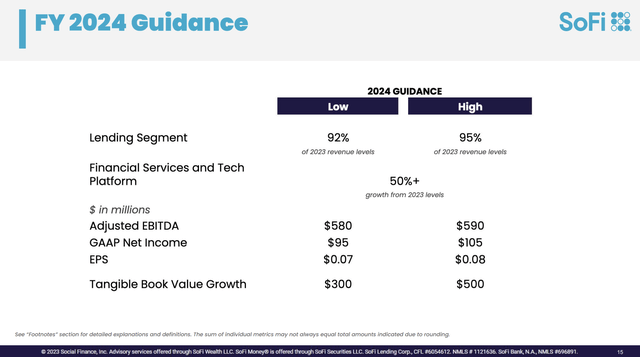

The fintech entered 2024 expecting another year of solid growth, with the potential for the student debt market to reopen and an opportunity to expand their mortgage business. Following Q4’23 earnings in late January, SoFi guided to strong growth for the year, and these targets weren’t even the big guidance offered up by management.

Source: SoFi Q4’23 presentation

The company even guided to weakness in the Lending segment, with revenue of only up to 95% of the 2023. All of top line growth was forecast to come from the Financial Services business and the Tech Platform due to management refraining from growing the loan book.

SoFi has constantly offered up conservative guidance in the indication that 2024 might repeat. The original 2023 guidance was for revenues of only $1.93 to $2.0 billion, and the company ended up hitting $2.1 billion for 35% growth.

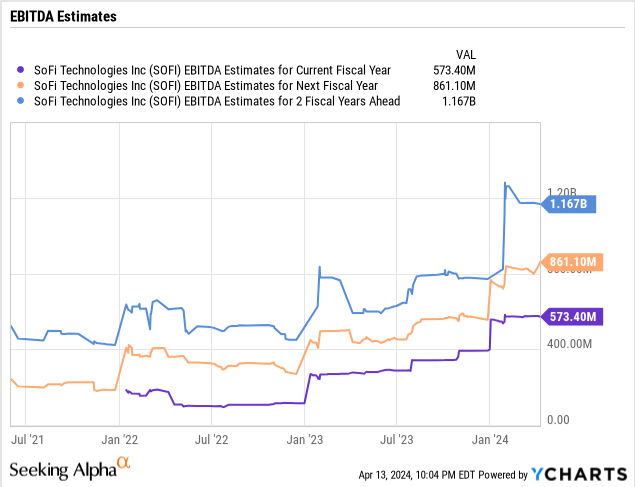

The more important targets, again ignored by the market, were the big jump in adjusted EBITDA and the growth in tangible book value. The market has become obsessed with GAAP EPS, but this metric is virtually worthless to a company growing TBV by $300 to $500 million.

SoFi guided to 2023 adjusted EBITDA of $270 million and actually hit $432 million. The company is now guiding to nearly $600 million for 2024, yet the market is valuing the stock based on a fraction of the targeted growth rate of 35%.

As a refresher, SoFi provided some very dire economic views to underpin the 2024 guidance as follows:

- GDP contraction in 2024 (Conference Board forecast nearly 1% trough growth)

- Unemployment jumps above 5%

- Fed cuts interest rates 4x (Fed increasing moving to 0 rate cuts)

- Fed funds rate ends year at 4.5%

As with 2023, SoFi based 2024 guidance on a dire financial situation that already appears unlikely before the fintech reports Q1’24 results on April 29. The Fed might not actually cut interest rates this year following solid GDP and hotter than expected inflation reported last week.

The more important guidance hidden in the Q4’23 earnings call was for substantial growth targeted through 2026.

- Compound annual revenue growth of 20% to 25%

- GAAP EPS of $0.55 to $0.80

- 20% to 25% GAAP EPS growth beyond 2026

In essence, SoFi continues to expect big growth over the long term while constantly guiding towards weak economic numbers in the short term. Note, all of these growth targets excludes the opportunity to invest in the business and launch major new products as follow:

- SME business checking

- SME business lending

- Broader asset management business

- Insurance

- Broader credit card portfolio

- New technology verticals

- New geographies

Said another way, SoFi has a long roadmap to new product launches along with still growing the existing member base. The consensus estimates have revenues already reaching $3.4 billion in 2026 and the targets aren’t for 20%+ annual growth and don’t factor in new product launches.

Yet, the stock only has a market cap of $7.7 billion while adjusted EBITDA is set to reach $1.2 billion by 2026 based on conservative targets. SoFi trades at sub-10x 20225 EBITDA targets for a company with vastly faster growth rates.

Takeaway

The key investor takeaway is that SoFi isn’t being valued accurately based on growth rates, despite a history of strong growth. The market constantly reads negatively into corporate decisions before understanding the sound financial reasons.

Investors should use the weakness to load up on SoFi currently trading at a vast discount to growth rates and earnings power. As highlighted in previous research, adjusted EBITDA approaches adjusted profits and the stock trades at less than 10x forward targets.

Read the full article here