Aerial Nevada desert at Thacker Pass

Introduction

My email box and phone blew up last week with friends and family forwarding the big news of Lithium America’s (LAC)(LAC:CA) huge caldera-hosted lithium mine in northern Nevada. ‘Have you seen this?’ and ‘Is this one of the companies you’ve been talking about?’ they asked. Yes, and yes was my reply. Lithium America’s Thacker Pass development, a mine that has been in the making for over twenty years and been very publicly discussed in various news media had just been taken to a wider audience with a wave of coverage in the national media. Finally, a company that I’d been blabbing about endlessly and traded for four years was now finally on the minds of these friends and relatives. Apparently, my nonstop talking about lithium as a key element in EV batteries among other trends in energy storage took some third-party confirmation to sink in.

However, as boring as I’ve been blathering on about lithium mining stocks, I couldn’t be satisfied with being ahead of the curve on lithium in general. After all, lithium prices have declined precipitously from record highs, so it has been a stock-pickers market for lithium mining stocks.

Back to Lithium Americas. ‘Yes, and yes,’ I said, but then I added a big new reveal: There’s an early-stage lithium company, Surge Battery Metals (OTCPK:NILIF)(TSXV:NILI:CA), that looks to be sitting on a lithium deposit that checks all the boxes that Thacker Pass does, and is arguably better, but it is trading at 1/10th the value or less. This company’s property is also in Nevada, ranked the number one mining-friendly region in the world by the Fraser Institute. They’ve drilled some remarkable holes judging by lithium content, strike length, and initial geology and metallurgy. So remarkable that: the Chairman of the company (a respected figure in the world of lithium, mining and finance); a Director (former Rio Tinto executive and geologist); and the Chairman of another public lithium mining company that became a strategic investor (American Lithium (AMLI)(LI:CA)) all had a similar initial response: Surprise, intrigue and sometimes head-shaking disbelief.

When the news release came out on some drill results for Surge Battery Metals a few months ago we kind of shook our heads and thought well that’s kind of interesting, and there’s a whole different caldera over there and we were just surprised and then we started to do some homework and ended up signing an NDA and then got into some of the met work and then because we’ve spent seven years in Nevada understanding the rocks and understanding the Metallurgy and the geology we were able to sort of dig in there quite quickly and we were really intrigued…”

– Andy Bowering, Chairman of American Lithium about his company’s approximate 10% stake in Surge Battery Metals (beginning at 11:34)

Despite the reservations I had at first, it just sounded too good to be true. Well, somebody’s got a decimal point off here and got to do some due diligence on it and looked into it and lo and behold, they hadn’t got a decimal point off. It just is really surprisingly high grade.”

– Iain Scarr – Director, Surge Battery Metals. (Source: Interview Transcript)

We had a really successful exit strategy at Millennial Lithium we got taken over by Lithium Americas for 500 Million dollars last year…you know I wasn’t really too keen to get back involved…like anything in life everything’s work…I looked at a number of projects that came my way after Millennial Lithium and none of them really stood out as having the potential to be of size and of scale to interest an acquirer until I saw Surge Battery Metals and what really intrigued me about this company was the early stage exploration results from the previous year’s drilling and they just caught my eye because the grades were much higher than all the comparable companies in the lithium space.”

– Graham Harris – Chairman, Surge Battery Metals (Source: Corporate Video

I’m going to assume that readers are familiar with the lithium space. I’m not going to discuss the chemistry of lithium-ion batteries, and I’ll expend little to no ink on the differences between the three general types of lithium mining, hard-rock, brine and sediment/clay. The reason I’m going to skip all that for now is I want to get this article out rapidly because I think after last weeks big pullback after a breakneck run, that Surge Battery Metals warrants a strong buy recommendation. I am convinced of this opinion based on the current supply and demand picture, my experience investing in lithium stocks and investing in general. I think that Surge Battery Metals will be acquired for at least five times the current market capitalization in relatively short order. I want this article to serve as a stake in the ground at this point in time so I get the intangible “credit” for having informed a wider audience about Surge Battery Metals, hopefully to our mutual success.

Of course hope is not a reliable investing strategy. In my long investing experience though, simple comparative economics is quite reliable. That is just taking one product, company, or resource project, and measuring it against another more established and higher valued one, and determining whether the former is undervalued based on the qualities of each project and the market capitalization of the companies being compared. I’ll do that with Surge Battery Metals’ Nevada North Lithium Project.

About the Nevada North Lithium Project

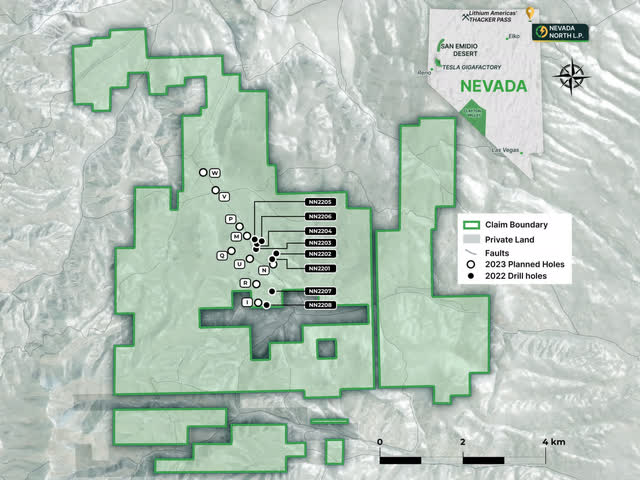

The Nevada North Lithium Project (NNLP) is in Northeast Nevada in Elko county. It now encompasses 725 mineral claims, a total area of 22.45 square miles, and is open in multiple directions. The expanded size model is over 8.5 times larger than just this past February 2023 based on the latest results of the drilling campaign, soil samples and geophysics.

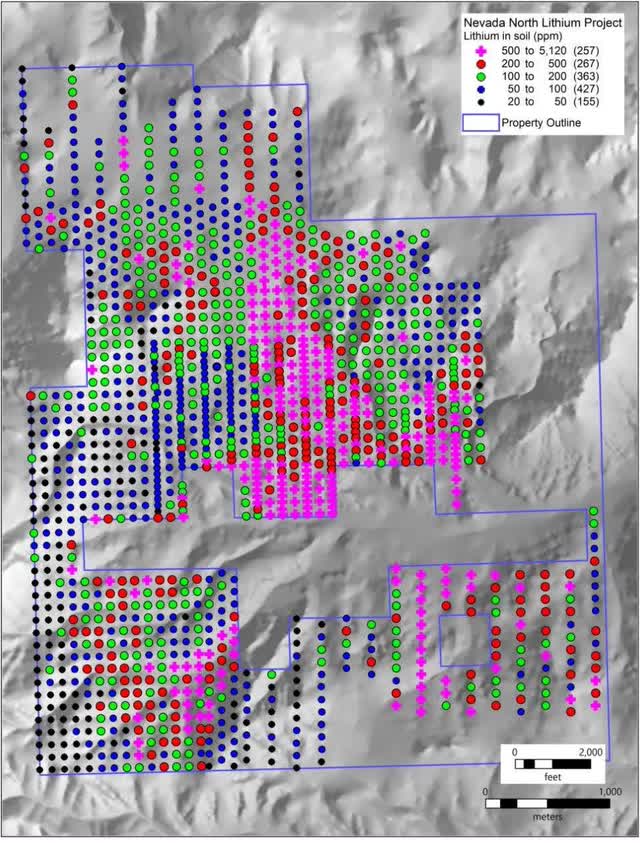

What first caught my attention about Surge’s NNLP last November 2022 was the below map, showing geologist Alan Morris’ area-wide soil sample results across the original footprint of the project. Stunningly, the pink/purple regions reflect lithium values at the surface from 500 to 5,120 parts per million (ppm).

Surge Battery Metals’ Surface Soil Samples Map (Surge Battery Metals’ Website)

Drilling Results So Far

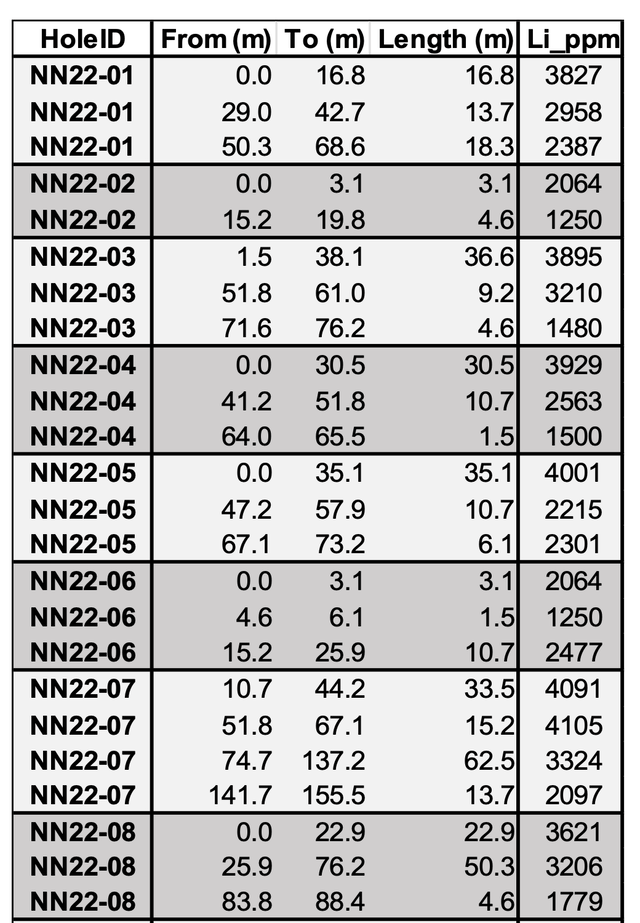

Not only are lithium readings at the surface like this extremely rare, the whole economics of a project can get a huge boost if the surface readings are confirmed to run deep. And they do, as confirmed by a 2022 drilling campaign that posted the results below:

Surge Drilling Campaign 2022 Results (Surge Battery Metals Corporate Deck)

As you can see, these results are extraordinary in terms of grade and strike length, and rival the best results of clay/sediment hosted lithium anywhere in North America. Some highlights are the over 100 feet of 4001 average ppm lithium in hole 5 beginning right at the surface, and hole 7 which boasts over 330 feet of lithium mineralization ranging from 3324 to 4105 ppm lithium.

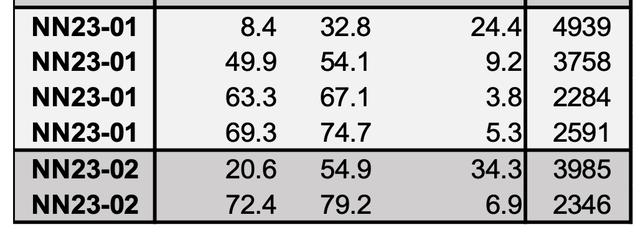

So far during the current drilling campaign, two holes assays have come back from the third-party lab and have produced the following results:

Surge Battery Metals 2023 Drilling Campaign (Surge Battery Metals Corporate Deck)

Here in NN23-01 we have about 75 feet near surface of pay at a whopping 4939 ppm lithium. According to Surge Battery Metals, the shallow zone includes lithium content of up to 8,070 ppm Li, which is apparently the highest ppm in Nevada ever confirmed by a lab.

NN23-02 continued to expand the size of the project to the northwest, as an 820 foot step-out, and contained one layer of core length of over 100 feet and a remarkable 3985 ppm Li average.

About eight more holes have been drilled, including the deepening of a few previously drilled holes upon further indications of additional highly prospective zones of lithium at lower levels.

Surge Drilling Map 2022 and 2023 (Surge Battery Metals’ Website)

Comparing Surge’s Nevada North to Lithium America’s Thacker Pass

If the Nevada North Lithium Project appears to be as significant in size, grade, ease of lithium extraction, and level of impurities as Thacker Pass, the NNLP should be valued the same as Thacker Pass. If the NNLP proves to be of greater significance in the majority of these factors, it should be valued higher than Thacker Pass. This is the basic thesis.

However, we certainly need to add a lot of points to Thacker Pass for its stage of operations including finalized permitting and approval, finalized mining flow sheet and plan of operations, defined metallurgy, and financing. Lithium Americas has been at this a long time, and is clearing ground and commencing operations. They are much farther along, and there is a significant value attributed to project stage by the Market.

Once Lithium Americas finalizes it’s split into two entities, one which holds the South American assets and the other which holds the North American assets, we will know how the Market values Thacker Pass. Fellow Seeking Alpha contributor Jaberwock Research wrote a comprehensive article with a valuation estimate on the separated entities. They ascribe a value to Thacker Pass of $4.009 Billion, discounted by .7, excluding a 636 Million investment from GM, of which half has been injected so far. They give a value to the South American assets of $2.354 Billion post cash of $167 Million and debt of $279 Million. Because the Market is currently valuing the combined company at $2.72 Billion in Market Cap, which is less than half of Jaberwock’s discounted all-in current value, I’ll use their ratio of 70%/30% in favor of Lithium America’s North American assets. This comes to about $1.9 Billion for Thacker Pass in terms of current Market Cap.

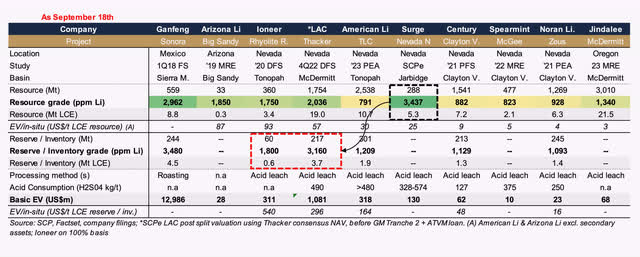

On to the comparison. Here is a table of the most important clay/sediment hosted lithium deposits in North America:

Important North American Clay/Sediment Hosted Lithium Deposits (Surge Battery Metals’ Corporate Deck)

From the table above, we can see that Surge’s NNLP has higher average grades than even stellar Thacker Pass, averaging 3,437 from its drilling campaign thus far.

In its initiation of coverage, the analysts at SCP Resource Finance (previously known as Sprott Capital Partners) estimates, based on last year’s drilling alone, a resource of 2.5-3Mt LCE @ 3,437ppm Li. They believe that this season’s just completed drilling could lift the resource towards 4-6Mt LCE. SCP further sees blue sky potential of the NNLP at 15Mt LCE.

Upcoming holes are being drilled deeper, to up to 1000 feet, and previously drilled holes are being deepened after indications of deeper targets. 15Mt LCE could even be conservative in my opinion, and we’ll find out soon from the assays of these deeper targets.

‘How can one make an estimate like this with only the assays from 10 holes?’ some will protest. Fortunately, the nature of clay-hosted lithium deposits gives geologists confidence, as clay-hosted deposits often show remarkable consistency and continuity across a wide area.

Thacker Pass sits in the McDermitt Caldera, an ancient lake inside that formed inside a collapsed volcano which collected lithium enriched sediments from various geologic occurrences over millions of years — including of course the volcano’s initial eruption — constrained by the volcano’s edges. Over time these sediments became further enriched with lithium as detailed in one of the papers principally authored by Lithium America’s Thomas Benson, Hydrothermal enrichment of lithium in intracaldera illite-bearing claystones, that garnered a lot of well-deserved attention in the press recently.

The high grades of Li-bearing clay being found at the NNLP are similar if not higher than the grades found at Thacker Pass, and the regional rocks have been described as of similar age and composition to the McDermitt Tuff soils that host lithium at Thacker Pass. The NNLP sits in the site of the Jarbridge Caldera, and it appears from the location and geology that the same factors that enriched the lithium-bearing clays at Thacker Pass could also be responsible for the NNLP’s record-breaking levels of lithium ppms.

Further, in the recent interview with Surge director Iain Scarr, he mentions that there is more Hectorite present in the soils of Thacker Pass than present at the NNLP, hence extracting the lithium from NNLP should be less complicated and less costly.

Speaking about soils, the SCP analyst points to a beneficially low magnesium content (2-4%) and the presence of coarse calcite crystals which aid in extraction/purification efficiency.

Another key factor in mining is ‘overburden’, which is simply how much relatively worthless rock and dirt sits above the valuable resource that must be removed to get to the good stuff. As mentioned above, the majority of Surge’s drilling so far has revealed the very best grades at the surface, with little to no overburden. Compare this to Thacker Pass, which finds itself in the opposite position. At Thacker Pass, the best grades are generally at least 100 feet below the surface and the lesser grades are at the surface. Overburden equals additional cost. Surge’s project is blessed with high grade at the surface in the resource area drilled so far.

To sum up the comparison, Lithium America’s Thacker Pass mine is being valued in the Market right now at $1.9 Billion before the second $300 Million+ cash infusion from GM, assuming the value of the entire company pre-split is 70% in favor of Thacker Pass. We will find out this week, perhaps before this article comes out. Regardless, some Seeking Alpha contributors see a value of Thacker Pass of up to about $5.7 Billion (excluding the $636 Million from GM)

Let’s be a bit conservative and give Thacker Pass a current value of $1.5 Billion. Surge Battery Metals has a current market cap of about $109 Million U.S. dollars, and a fully diluted market cap of about $140 Million U.S. dollars.

That is a discount of 10 to 15 times Lithium America’s flagship asset. In doing this comparison, I asked myself what the likelihood is that the NNLP becomes a mine. Considering all of the positives and the comparison that at the very least gives the NNLP an equal value if it becomes a mine after it is proved out by the requisite amount of drilling, I have no doubt that it does become a mine. It will probably not be owned by the same corporation at that point, as I can see Surge Battery Metals being acquired for a substantial premium in relatively short order.

After all, Lithium Americas reportedly had numerous competitors vying to take the stake that GM ended up winning. The U.S. Administration has recognized the urgency of a domestic supply of lithium and other critical energy metals, and plenty of companies are finding out the hard way that some nations are looking to nationalize or further control lithium projects. Case in point: the Sonora Lithium project in Mexico. The government of Mexico just revoked a number of concessions from Chinese giant Ganfeng Lithium, in a move that could delay another large source of lithium to a world that is estimated to be going into deficit for years.

Surge Battery Metals’ Management

When investing in the mining sector, it’s often wise to bet on the repeat performers. Their contacts, geological experience and instincts come in especially handy in the relatively small community of lithium experts. Its a small community because for a very long time, lithium wasn’t worth a whole lot. How times have changed.

The Chairman of Surge Battery Metals is Graham Harris, an experienced executive and financier who sold his last company, Millennial Lithium, to none other than Lithium Americas for $490 Million U.S.

The President and CEO of Surge is Greg Reimer, who before Surge was EVP of Transmission and Distribution at British Columbia’s electric utility BC Hydro, serving 4 Million customers. He previously served as Deputy Minister of Energy, Mines and Petroleum Resources, and Chair of the BC Oil and Gas Commission.

Director Iain Scarr is a geologist with more than 30 years at Rio Tinto, including serving as Commercial Director and VP of Exploration.

Director Dr. Vijay Mehta holds a BSc in chemistry and a PhD in flotation technology. A holder of numerous patents involving lithium processing and extraction, Dr. Mehta is a world-renowned expert in lithium mining, extraction, and processing.

Director Ted O’Connor is EVP at American Lithium Corp. and the board representative for American Lithium’s investment in Surge Battery Metals. He is a professional geoscientist and brings more than 30 years of experience in the exploration industry to the Company, including working directly on American Lithium’s TLC Claystone Project in Nevada.

Financials/Share Structure

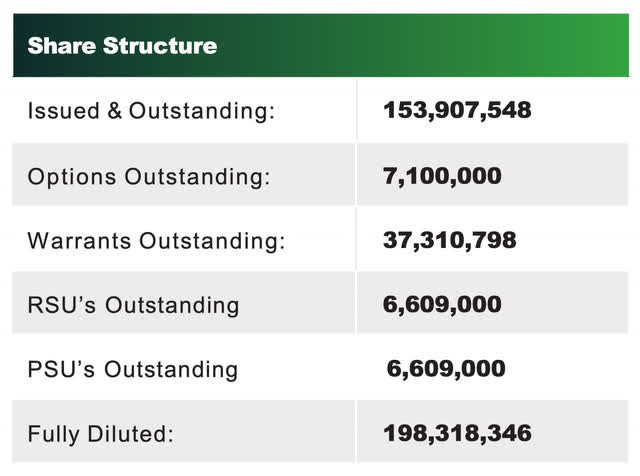

Here is a rundown of Surge’s share structure from their most recent corporate deck:

Surge Battery Metals’ Share Structure (Surge Battery Metals Corporate Presentation)

The Company raised about $7 Million dollars in June 2023, mostly from American Lithium, which has funded their recent drilling and exploration campaign. They reported about $9.6 Million on the balance sheet at the end of June. Warrants attached to that financing should bring in some more money to the company if American Lithium chooses to increase its stake in Surge, which I expect them to do. Other financing will of course be necessary in the future for Surge to keep up the pace of drilling. Considering Surge’s prospects and the attention coming to lithium in Nevada, I think financing will not be a problem, and could come from many sources, including another strategic investor.

Upcoming News

As detailed previously, Surge just concluded its second drilling campaign, and has released results on two of them. There are about eight yet to be released after they are analyzed at the lab, including some that have been re-entered with a rig that can handle greater depths.

Other news could relate to additional land acquisitions, additional strategic investors, and perhaps additional site visits another global automaker, which the CEO described after the initial drilling results were released.

Then, the Maiden Resource Estimate (MRE) will be released, estimated by the company variously to be arriving as early as November 2023 but at the latest Q1 2024. More recently, company representatives have said that Q1 is more likely, to allow the incorporation of the results of the whole second drilling campaign.

Risks and Uncertainties

Below is my own standard list of the main risks I consider specifically when considering an investment in junior mining stocks, beyond the general risks inherent in any public company investment:

- The size and quality of the mineral resource must be proven via measurements and testing before being considered profitable to extract;

- The intended extraction method might be difficult, costly, or even futile;

- Permit grants and operations of the mine are subject to policies of the government where the resource is located;

- Demand for the underlying resource might fail to materialize or drop;

- Overproduction of the resource might cause oversupply in the marketplace;

- Local environmental considerations might make mining difficult or impractical;

- There might be local community opposition to the project that prevents or interrupts mining.

What balances some of these standard risks in Surge’s case is Lithium America’s hard-fought but trailblazing success. They had rough patches along the way, had court fights and doubters of the technology behind lithium extraction from clay/sediment, but emerged successful and are rumored to be close to a $1 Billion loan from the U.S. government to fund mine construction.

Surge is the beneficiary of the “Second Mover Advantage”. By following Lithium America’s playbook where it was successful and avoiding the minefields where it had difficulties, Surge could really expedite the timeline to a producing mine, or a buyout. Who better to guide the team than Chairman Graham Harris who led his company’s buyout by Lithium Americas, and CEO Greg Reimer (who rapidly focused Surge on the NNLP and started to assemble a crack team when he saw what they had in the ground)? Chairman Harris has done this before, and I was a beneficiary since I owned stock in Millennial Lithium.

One final point concerns the price of battery-grade lithium. Spot prices are volatile, and reflect short term supply and demand considerations, but most lithium is purchased on long-term contracts. Some might think that currently depressed prices in the spot market are a sign of a surplus of lithium. Maybe if viewed week-to-week, but the long term demand picture is extremely bullish, and might even get desperate as countries increasingly look to protect their own national lithium interests, cancel concessions, and various mines get delayed or cancelled such as Rio Tinto’s Jadar in Serbia and Sonora in Mexico.

Analysts at Macquarie have recently argued that lithium supplies have been depleted now to the level where prices began to soar the last time.

Conclusion

Sometime in the near future, but within a year, I expect Surge Battery Metals to be acquired by one of the big names in lithium such as Rio Tinto, Albermarle, BHP, Lithium Americas, or even a specialty chemical conglomerate, auto manufacturer or oil major. There are a lots of contenders out there, and if (I think the operative word is when) Surge’s official MRE confirms the highest-grade clay-hosted resource in North America, which has minimal overburden and favorable extraction parameters, I predict Surge’s share price will ramp up further to reflect greater awareness of this remarkable project.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here