The four themes

There are four themes shaping the S&P 500 (SP500) performance over the near term:

- First, the GenAI bubble burst. The tech mega-caps have been heavily investing in Gen AI, but it seems like the ROI in Gen AI capex might be too low, at least over the near term. In addition, based on Nvidia’s latest earnings report, the growth is slowing, which does not justify the lofty valuations.

- The second theme is the unfolding Fed-growth-inflation story. Specifically, based on the weakening labor market, it seems like we could be facing an imminent recession. Thus, the Fed is expected to aggressively cut interest rates over the next 12 months. Given that we are not in a recession yet, some hope that the Fed’s cuts would actually avoid the recession. That’s the soft-landing scenario, where the key assumption is that inflation continues to fall towards the 2% level to allow the Fed to cut.

- The unfolding geopolitical situation. We are currently facing a severally escalating geopolitical situation in the Middle East and Russia, and both situations could spread to become regional wars, involving the NATO.

- The Yen carry trade blow-up. The Fed is expected to cut interest rates, while the Bank of Japan is still expected to increase interest rates, which could boost the value of the Japanese Yen, and thus, force the hedge funds who borrowed the Yen to liquidate their Yen-financed positions.

The interplay between these themes will determine the price action of the S&P500 over the near term, or over the next 6 months.

The key assumptions are:

- The geopolitical situation will remain under control to the point that the price of crude oil (USO) does not spike. The spike in crude oil price could increase inflation, and prevent the Fed from cutting interest rates, despite the weakening labor market – this would be stagflationary, and, thus, very negative for the stock market. However, this is also a situation that can be controlled, at least until the US November elections.

- The BOJ and Fed can keep the rise of the Yen under control, and thus another episode if the Yen carry trade blow up is unlikely.

- The AI bubble bust can be delayed as long as the broad sentiment remains positive, and at least until the next earnings season. The AI tech mega caps will start reporting in mid-October, until then, the Nasdaq 100 (QQQ) could only gradually decline, and even stay flat.

It’s all about the Fed now

Thus, the key theme that will be driving the markets over the near term will likely be the Fed and the related growth-inflation environment.

The Fed is expected to start cutting interest rates in September, and cut at each meeting in 2024, and continue cutting in 2025 down to around 3% in Federal Funds rate.

These expectations are consistent with a recession – that’s the only time when the Fed actually cuts interest rates by over 2%. Thus, if these expectations are correct, we should be getting more data confirming an imminent recession, especially in the labor market.

The most recent data has not confirmed an imminent recession yet.

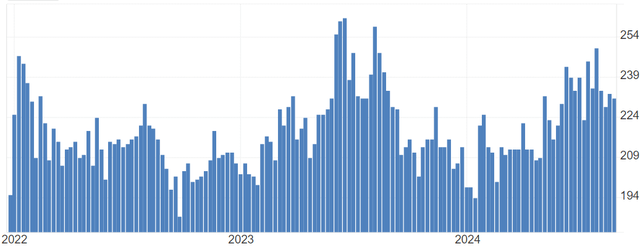

The initial claims for unemployment have risen to touch the 250K level, but over the last 3 weeks, the claims fell to the 230K level. The trend is still to the upside, so more weakness is expected. However, over the last 3 years we had two prior episodes when the claims spiked to the 250K level, and subsequently fell back to the 200K level. In these cases, the recession was avoided. What will happen in the current situation?

To have a clear signal of an imminent recession, the claims must spike above 250K level and continue rising.

Claims (Trading Economics)

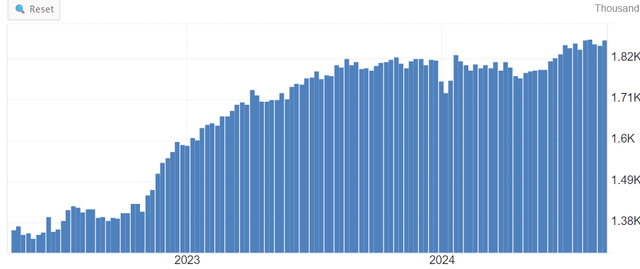

Similarly, the continuing claims for unemployment are at the 3Y high level, but have stalled over the last 3 weeks. We need to see the spike above the 2M level to get confirmation of an imminent recession.

Continuing Claims (Trading Economics)

The labor market is weakening, and the Sahm Rule has been triggered – the unemployment rate has increased to 4.3%, well above the low point of 3.4%. However, at this point, the increase in the unemployment rate is mostly due to an increase in the labor supply – due to immigration and an increase in participation, and not due to job losses. We need to see actual job losses to confirm a recession, and that’s not the case at the moment.

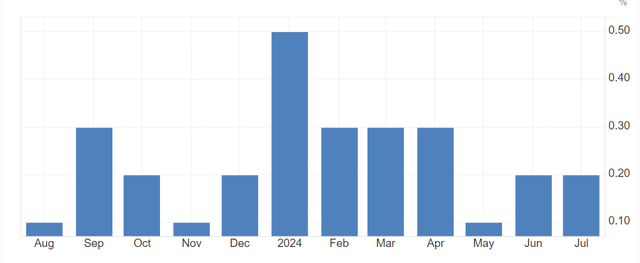

The next issue is inflation. The Fed needs to have confidence that inflation is falling towards the 2% level to be able to start cutting interest rates in September. The core PCE has been “stuck” at 2.6% for the last 3 months, and the July monthly core PCE inflation rose 0.2%.

Based on the base effects, the core PCE is likely to remain at 2.6% until the end of 2024, and really start falling in 2025 towards the 2% level, which could be reached by next summer. That’s assuming that core PCE continues to rise by 0.2% per month.

Core PCE MoM (Trading Economics)

The problem for the Fed will be if the unemployment rate stays at 4-4.3%, meaning all entrants to the labor market get hired while no jobs are lost, and thus, the shelter inflation fails to moderate, as the demand for housing continues to increase. Thus, this could boost the core inflation rate and prevent the Fed from cutting. The Fed’s Inflation Nowcast is predicting that core CPI could reach 0.3% in August. This would make it more difficult for the Fed to cut in September.

Implications

The base-case mid-term scenario remains that we are facing an imminent recession, and thus the S&P500 is facing a recessionary bear market, which accelerates the Gen AI bubble burst. However, we need data to confirm this theme.

If the labor market data remains solid, and the Fed still starts cutting interest rates in September, the positive sentiment can keep the market from falling, at least until the next earning season.

Thus, over the next few weeks, it will be all about the growth/inflation data, and the Fed. That’s assuming no geopolitical shocks, which is a weak assumption.

Read the full article here