Thesis

In my previous analysis of Hudbay Minerals (NYSE:HBM), I forecasted that the company’s share price (then at $4.55/share) was forming a falling wedge pattern due to concerns about Chinese copper demand and the repeated rate hikes announced by the Fed at that time (to control growth-led inflation) and that it was likely to find support within the range of $4.25-4.35/share over the next three months. As seen in HBM’s recent price chart below, the stock touched the indicated support levels (at the mid-point range of $4.30) twice during the three months from March 2023 to June 2023.

HBM’s 1-Year Technical Price Chart – Source: Finviz

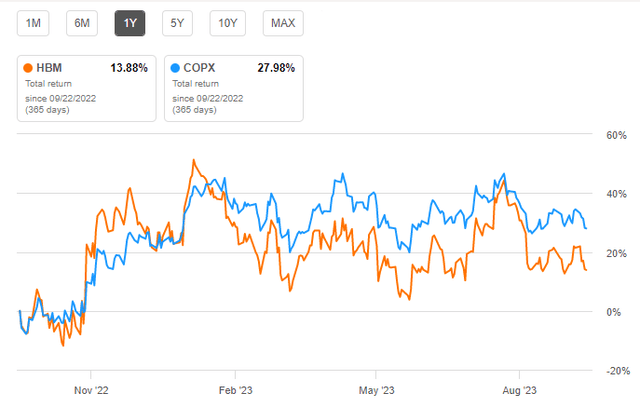

HBM’s 1-year technical price chart’s “peaks and troughs” form an upward wedge pattern, indicating that the share price could move north from the current levels. At the time of writing, HBM’s last traded price of $4.65 was ~7% below the mid-point value (at $4.98) of its 52-week range (between $3.62-6.34) and ~8% lower than its 200-day SMA (Simple Moving Average) of $5.09. Besides, HBM’s 1-year total price returns (of ~14%) have underperformed the returns (~28%) of its benchmark ETF, Global X Copper Miners ETF (COPX), by ~50% (note that HBM comprises 2.16% of COPX’s portfolio). Check the chart below.

1-Year Total Returns – HBM v/s COPX – Source: Seeking Alpha Premium

While all the above technical indicators indicate that the stock is likely to witness an upside, the fundamentals are more important. This article discusses the permitting challenges facing HBM’s Copper World project (in Arizona), HBM’s recent acquisitions that strengthen its Canadian footprint and partly offset the impact of permitting risk in Arizona, the Peruvian risk factor, the turbulence in copper prices, and HBM’s balance sheet (which remains strong despite a significant debt). The above discussion will help analyze whether HBM can provide attractive share price growth over the near-term, medium-term, and long-term investment horizons. Let’s get into the details.

HBM Operates in Tier-1 Jurisdictions, But Risks Remain

The term ‘Tier-1 jurisdiction’ in the mining industry refers to relatively low-risk mining regions with stable economies, investor-friendly mining/taxation policies, fair and transparent permitting processes, etc. Meanwhile, the term ‘Tier-1 asset’ refers to an asset with attractive mining dynamics, including significant high-grade reserves (and resources), long-life mines, low production costs, accessibility to infrastructure, etc.

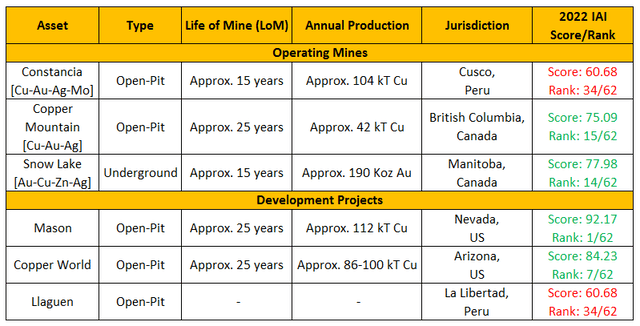

The following table highlights the key characteristics of HBM’s mining assets (including ‘producing’ mines and ‘future’ projects). In this table, the IAI score/rank refers to the relative value/rank assigned to a mining region in the Investment Attractiveness Index (or IAI) included in the Fraser Institute’s 2022 Annual Mining Survey. This score broadly considers the jurisdictional risks based on multiple metrics (the full report can be accessed here).

HBM’s Portfolio Key Characteristics – Source: Author

Based on the information in the above table, we may conclude that HBM is indeed operating a portfolio of geographically diverse assets comprising base/precious metals, and most of these assets are located in a Tier-1 jurisdiction (such as the US and Canada). However, there are exceptions to the general assumption that Canada/US are low-risk jurisdictions.

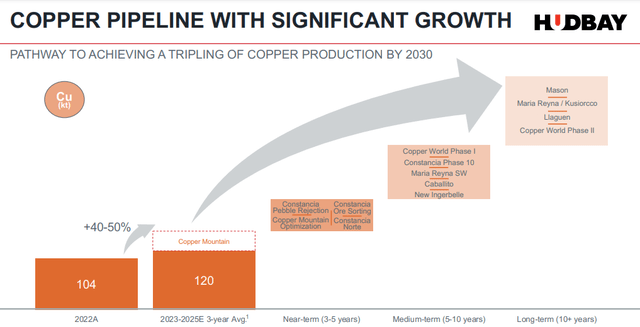

HBM’s timeline for organic growth in copper production from its existing/pipeline projects envisions the Copper World’s Phase-1 (or CWP-1) to become operational in the medium term (5-10 years).

Copper Production Organic Growth Timeline – Source: Presentation

Based on HBM’s recently released PFS (Pre-Feasibility Study) on CWP-1, the project entails the following key characteristics (including a few that changed from the earlier PEA):

- Expected annual copper production of ~92,000 tons, up from prior expectations of ~85,000 tons.

- Expected cash costs and sustaining cash costs of ~$1.53/lb and ~$1.95/lb deteriorated from prior expectations of ~$1.47/lb and ~$1.81/lb, respectively.

- CWP-1’s mine life is extended from 16 years to 20+ years.

- Deferral of construction of a concentrate leach facility to year 4 (and to be financed from the project’s operating cash flows) led to a reduction of initial project development capex from $1.9 BB previously to ~$1.3 BB (or ~$1.1 BB net of the impact of streaming agreement).

- CWP-1 is estimated to have an after-tax NPV of ~$1.1 BB using an 8% discount rate and assuming LoM average copper prices of $3.75/lb, and is expected to generate an IRR of 19%.

- CWP-1 is expected to create ~3,400 (direct and indirect) jobs and pay ~$850 MM in taxes over the LoM.

The good thing is that HBM will not require federal permits for CWP-1, only state and local-level permits. On the permitting front, it’s important to note that the US ACOE (US Army Corps of Engineers) has determined that there are no jurisdictional waters on the site of the HBM’s former Rosemont Project (located on the eastern slopes of the Santa Rita Mountains versus the CWP-1 which is located on the western slopes of these Mountains) and confirmed that HBM’s surrender of Section 404 Clean Water Act Permit was accepted and revoked. This decision also confirms HBM’s stance that the new CWP-1 was not connected to the previous federal permitting process related to HBM’s Rosemont Project, which was axed in 2019 by a Federal judge.

The bad thing is that the Federal judge’s ruling was upheld by an Appeals Court in 2022, shattering HBM’s hopes of building a large-scale copper mine on the Rosemont Project site. Moreover, local tribes (including the Tohono O’odham, Pascua Yaqui, and Hopi tribes) and a couple of environmental groups such as ‘Save the Scenic Santa Ritas’ are fiercely opposing any mining activity in the areas around the Santa Rita Mountains, and have challenged HBM’s mine development activities in Court. The mine’s opponents cite concerns such as the protection of sacred sites of the local tribes, the risk of extinction of some endangered species/destruction of wildlife and ecosystem linked with the Santa Rita River, destruction of the famous Arizona hiking trail, usage of significant water from the local watersheds, and the future environmental impact of dumping tons of mineral waste on the area near the mine site (a similar case was reported here, also in Arizona and on the same grounds as HBM’s CWP-1). Despite the opposition, HBM has laid some preliminary infrastructure at the project site (carving of roads and berms) and is awaiting state-level permits to make a construction and investment decision about CWP-1. Meanwhile, HBM expects to execute an agreement for a minority JV partner (by 2024) before it commences DFS (Definitive Feasibility Study) on CWP-1 (expected 2025).

So what’s at stake here?

A large-scale mining project (CWP-1) on the Santa Rita Mountains’ western slopes could become the US’s third-largest copper project and an essential supplier of US-based clean-energy metals. While HBM is gradually advancing on state-level permitting milestones for the CWP-1, the company’s inability to proceed with Rosemont mine’s development (despite securing some initial permits), the Copper World Project opponent’s determination to somehow block the mining activities through the involvement of the Courts and government agencies, and the fact that HBM has yet to find a minority JV partner for project funding, spells risk for this otherwise promising asset.

Acquisitions To De-risk HBM’s Mining Assets Portfolio

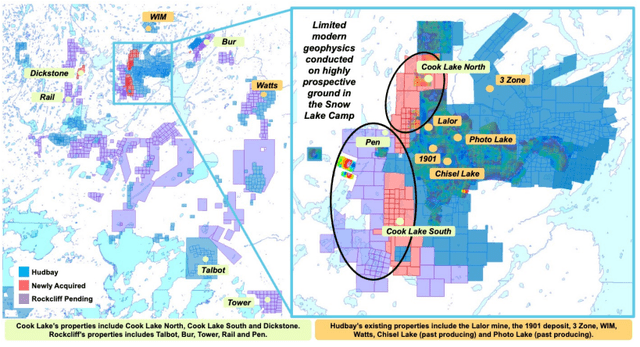

Rockcliff Acquisition: HBM recently completed the acquisition of Rockcliff Metals. The acquisition granted HBM 100% ownership over the Talbot project near HBM’s gold-focused Snow Lake operations. To quote HBM’s CEO on this occasion,

We are very excited about the completion of this logical transaction and the potential for Rockcliff’s deposits to extend the mine life and add further optionality to our operations in the Snow Lake region.

The Talbot deposit is estimated to host ~2,190,000 tons of Indicated resources comprising 2.1 g/t gold, 1.79% zinc, 2.33% copper, and 36 g/t silver (these resources translate to ~213 Mlbs of CuEq resource). Besides, the property is also estimated to contain ~2,450,000 tons of Inferred resources comprising 1.9 g/t gold, 1.74% zinc, 1.13% copper, and 25.8 g/t silver (these resources translate to ~161 Mlbs of CuEq resource). Moreover, the Rockcliff acquisition enables HBM to consolidate a highly prospective land package (including six additional 100% owned deposits) in the Snow Lake region.

Snow Lake Land Consolidation – Source: Presentation

In my view, the growth outlook of HBM’s Snow Lake operations is improving due to the following positive catalysts:

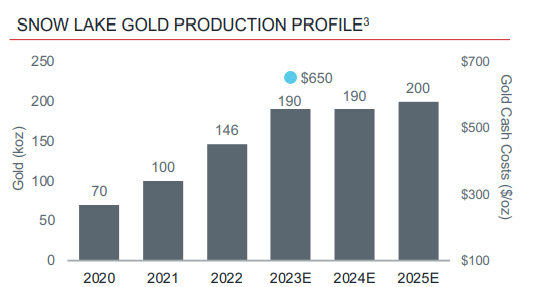

1) Snow Lake’s high-margin (operating margin: ~$1,200/oz) gold production is ramping up YoY, supported by the New Britannia mill that commenced production in 2021 and is dedicated to processing gold ore (the base metals ore is processed at the company’s nearby Stall concentrator).

Snow Lake’s YoY Gold Production Growth – Source: Presentation

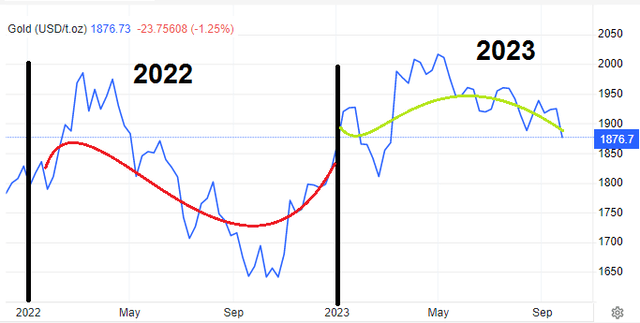

2) Average realized gold prices in 2023 are generally better than those in 2022. The prevailing gold price of ~$1,870/oz is impacted by a strengthening US$, but I see average gold prices over the near-to-medium term (say, 1-3 years) to remain within the range of $1,900-2,000/oz. Higher YoY gold prices will provide for higher operating margins in the future.

Average gold prices (2022 v/s 2023) – Source: Trading Economics

3) The long-term exploration upside from HBM’s Rockcliffe acquisition further improves the mining potential of HBM’s operations in the Snow Lake region.

4) The recent positive results of step-out drilling carried out ~500 meters northwest of the Lalor mine have led to the discovery of a high-grade Cu-Au-Ag zone, improving the mining economics of the Snow Lake region through a potential extension of the property’s mine life.

5) HBM’s consolidation of the Cook Lake properties in the Snow Lake region provides significant exploration upside in a potentially high-grade deposit (based on the historical results of the 60,000-meter drilling program carried out on these properties by previous owners).

Copper Mountain Acquisition: HBM completed the acquisition of the Copper Mountain Mining Corporation (which owns a majority stake in the promising Copper Mountain project in BC, Canada) in June 2023. During FY 2023, HBM expects to produce 150 kT of copper, of which 42 kT (or ~30%) will be produced at the Copper Mountain mine. The estimated production from Copper Mountain only incorporates production for H2 2023. In 2024, full-year production will increase the mine’s proportionate contribution to HBM’s total annual copper production (full-year production/cost guidance will be confirmed during Q4 2023 when HBM releases Copper Mountain’s updated technical report).

Unlike other acquisitions where mining companies typically acquire future projects, Copper Mountain adds a low-cost (low LoM strip ratio), long-life, conventional open-pit ‘producing’ mine to HBM’s portfolio. Copper Mountain is effectively a Tier-1 asset in a Tier-1 jurisdiction, which adds to HBM’s organic growth strategy in copper production. Besides, the prevailing depressed copper price environment (since early 2023) signifies the contribution of increasing YoY copper production toward securing higher operating cash flows.

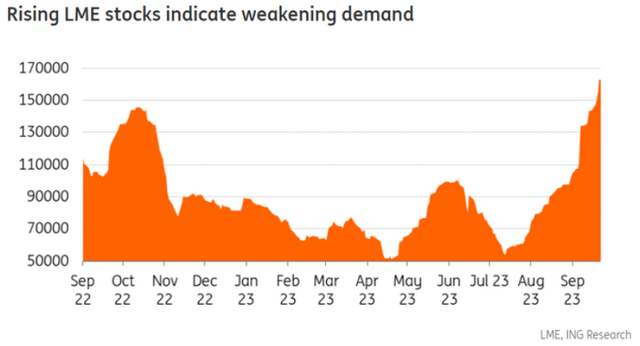

Depressed Copper Prices Since 2023 – Source: Finviz

Looks Like “Dr. Copper” Has Temporarily Passed Out

Notably, a slowdown in Chinese copper demand has adversely impacted global copper prices and resulted in the piling up of copper inventories, as reported by prominent metal exchanges. For instance, it’s reported that the London Metal Exchange’s global warehouses currently hold approximately 163,900 tons of copper (a ~50% increase from the inventory levels at the start of September 2023). Due to these macroeconomic factors, I expect near-term turbulence in copper prices.

Rising LME Copper Inventories – Source: ING Research

The Peruvian Risk Factor

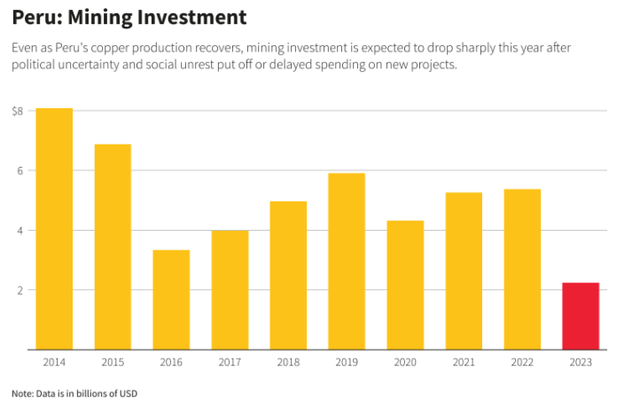

Besides the commodity price risk (and reward) factored in the share price, I believe the Peruvian risk factor also weighs on HBM’s investment thesis, as the company’s Peruvian Constancia mine is a significant ‘producing’ asset. Approximately 60% of Peru’s exports are derived from the mining sector, and the country’s reputation as the world’s 2nd largest copper producer (after Chile) comes with a price. Peru needs to sort out three problems impacting its mining sector simultaneously:

(1) Disagreement between mining companies and the Peruvian administration on a law limiting the use of contractual workers in the mining industry.

(2) The Government aims to streamline the environmental permitting process, which acts as a headwind in securing environmental permits for future mining projects in Peru.

(3) The above two factors lead to a significant drop in investment in Peru’s mining sector. Look at the chart below.

Investment In Peru’s Mining Sector – Source: Reuters

Although we cannot assess the quantitative impact (if any) of the above Peruvian challenges on HBM’s Constancia mine and the Llaguen project, it’s still worth noting these risks.

Balance Sheet Remains Strong Despite Rising Debt

HBM has maintained a strong balance sheet that increased from ~$4.33 BB (at the end of December 31, 2022) to ~$5.24 BB (at the end of June 30, 2022) primarily due to an ~$800 MM increase in Property, Plant, and Equipment, including the cost of strategic acquisitions (discussed earlier). The total long-term debt worth ~$1.37 BB appears to be a concern (net debt was ~$1.19 BB on June 30, 2022), as it increased by ~$186 MM during the past six months (net debt rose by ~$232 MM).

However, HBM’s robust liquidity position covers the outstanding debt well. On that note, the current portion of LTD is only ~$145 MM. In contrast, HBM had cash and equivalents worth ~$180 MM at the end of Q2 2023, an undrawn RCF (revolving credit facility) worth ~$184 MM (the undrawn RCF declined by ~$90MM, post Q2 end), and strong operating cash flows. Notably, HBM generated ~$95.8 MM in OCF during H1 2023, and I expect OCF generation to improve during H2 thanks to added copper (and gold) production from the Copper Mountain mine.

That said, I believe HBM’s balance sheet is strong enough (the company is targeting a net debt to EBITDA ratio of 1.2x) to provide the liquidity needed to support its medium-to-long-term pipeline projects.

Investor Takeaway

HBM is a diversified Americas-focused copper/gold producer whose recent acquisitions strengthen its operational footprint in Canada, paving the way for operational efficiencies/synergies and YoY production growth.

On the flip side, permitting uncertainties surrounding HBM’s promising Copper World (Phase I) project, the Peruvian risk factor, and depressed copper prices weigh on an investment thesis in the company.

Considering the above factors, we may conclude that while HBM’s organic growth prospects look promising over the medium-to-long-term investment horizon, the share price may only witness moderate growth in the near term. That said, I see the stock as a hold.

Read the full article here