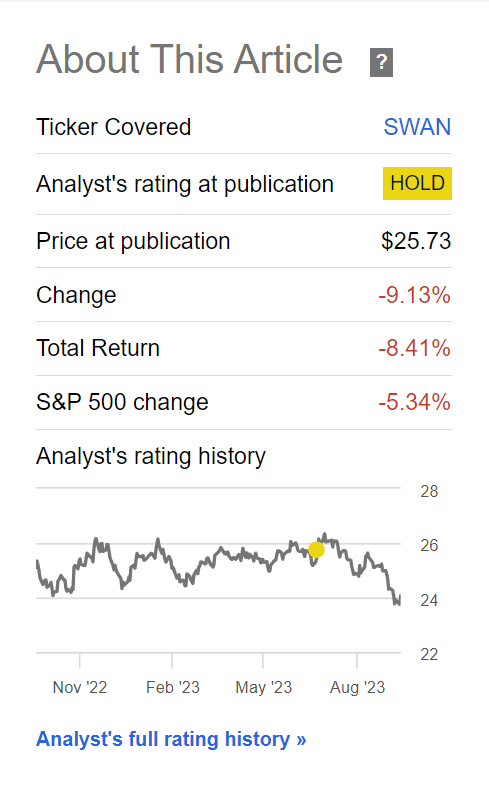

A few months ago, I wrote a cautious article on the Amplify BlackSwan Growth & Treasury Core ETF (NYSEARCA:SWAN), arguing investors should be cautious of overly engineered funds like the SWAN ETF.

The SWAN ETF markets itself as offering “participation in S&P 500 returns while seeking to protect against significant losses”. Unfortunately, I believe it introduced significant duration risk to investors’ portfolios that were not well advertised.

Since my article, the SWAN ETF has declined by over 8% in total returns, significantly worse than the S&P 500’s 5% drawdown (Figure 1). This poor performance is a replay of 2022, when the SWAN ETF significantly underperformed the S&P 500.

Figure 1 – SWAN ETF has declined by 8% since July (Seeking Alpha)

Why did the SWAN ETF perform so poorly, and what is the outlook for the fund?

Fund Overview

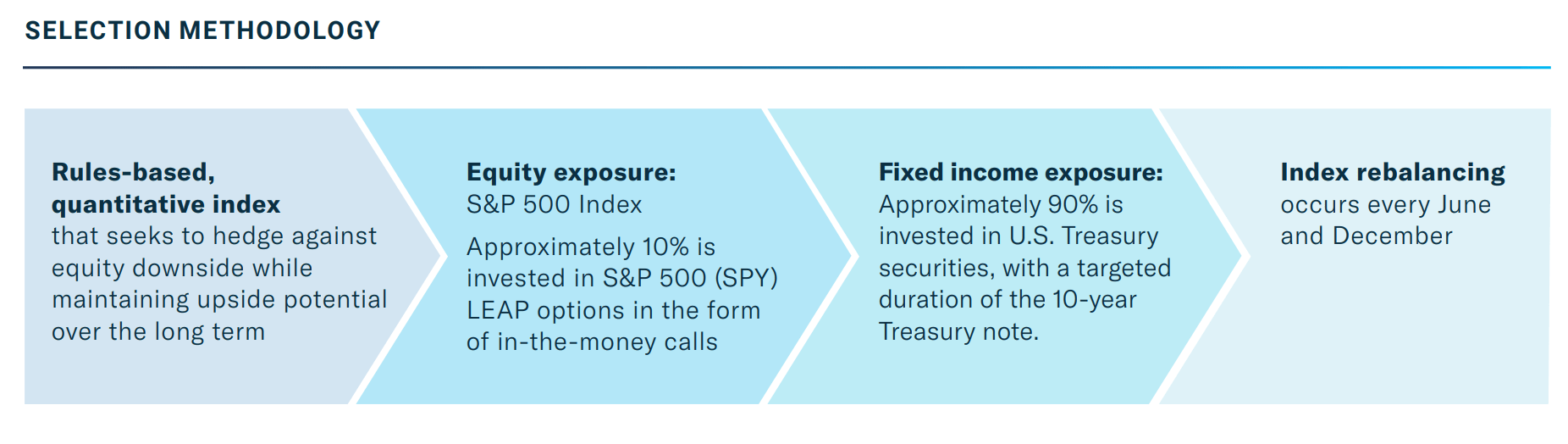

First, for readers not familiar with the SWAN ETF, the Amplify Black Swan ETF aims to provide equity-like exposure to the S&P 500 Index via LEAP options on the SPY ETF with 10% of the portfolio while ‘preserving’ capital with a portfolio of U.S. treasury securities on the other 90% (Figure 2).

Figure 2 – SWAN strategy (amplifyetfs.com)

The manager buys in-the-money (“ITM”) options with ~70 delta (for every 1% move in the underlying, the option value changes by 0.7%) with expirations of at least 1 year at the time of purchase. SWAN’s portfolio of treasury securities is aimed to provide protection against ‘black swan’ events.

In theory, since the SWAN ETF owns a portfolio of LEAP options, the most the fund can lose on the equity side is its 10% allocation to the options. Furthermore, the U.S. treasury portfolio is expected to mitigate overall losses during market drawdowns.

Stocks And Bonds Correlation Is A Grey Swan

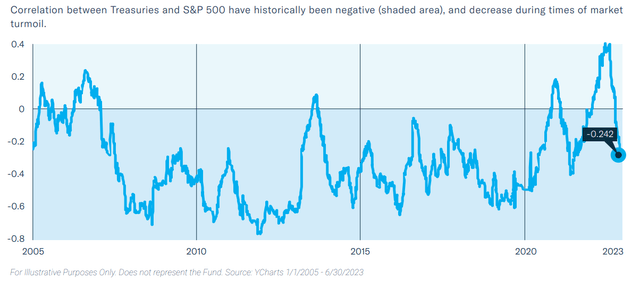

While the theory looks good on paper, the SWAN ETF’s strategy is based on the historic negative correlations between stocks and bonds that have been measured since 2005 (Figure 3).

Figure 3 – In recent years, stocks and bonds have been negatively correlated (amplifyetfs.com)

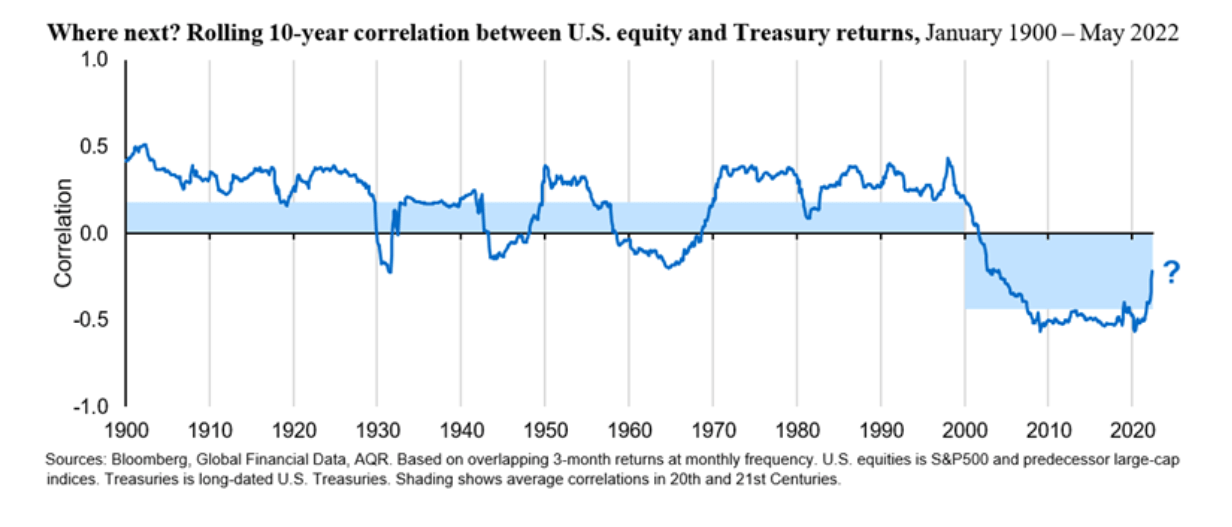

The ‘black swan’ SWAN fund was not properly designed for a ‘grey swan’ (predictable but unlikely) event of bonds and stocks being positively correlated and declining at the same time (Figure 4).

Figure 4 – Long-term correlation between stocks and bonds (Investment & Pensions Europe)

Historically, positive correlation between stocks and bonds have occurred for long stretches, especially during the 1970s and 1980s when inflation was raging and interest rates were raised to combat inflation (sound familiar?).

So the SWAN ETF, relying only on the past 2 decades of correlation to design its strategy, was bound to fail when the macro environment changes.

Performance Has Been Spectacularly Poor

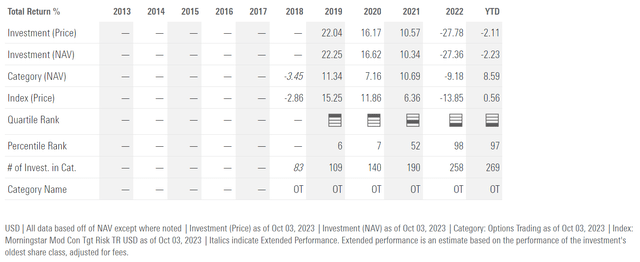

The SWAN ETF spectacularly failed in 2022, as the main driver of equity downside was rising interest rates. In 2022, the SWAN ETF lost more than 27%, which was far worse than the S&P 500’s decline of 18% (Figure 5).

Figure 5 – SWAN historical returns (morningstar.com)

SWAN’s negative performance can be explained by the decline in its portfolio of treasury bonds, as bonds are negatively correlated to rising interest rates.

In the last few weeks since the September FOMC meeting, we have seen a replay of 2022, with surging long-term bond yields and declining stock prices, as interest rates once again became the driver of equity market downside.

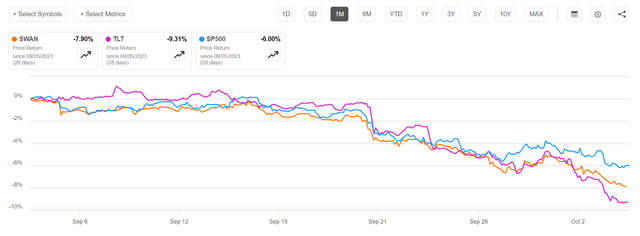

Figure 6 shows that a portfolio of long-duration treasury bonds, as modeled by the iShares 20+ Year Treasury Bond ETF (TLT), has declined by 9.3% in the past month while the S&P 500 has declined by 6%. The SWAN ETF has therefore declined by 7.9%.

Figure 6 – Treasury bonds and stocks have been declining in tandem (Seeking Alpha)

Where Is The Mention Of Duration Risk?

The SWAN ETF was not alone in its misery as many other ‘tail risk’ hedging strategies also failed in 2022, like the Cambria Tail Risk ETF (TAIL) that owns out-of-the-money (“OTC”) options on the S&P 500 Index and declined by 13.2% in 2022, offering no protection against the equity bear market.

However, my pointed criticism of the SWAN ETF is with its marketing, which claims to offer equity upside while protecting downside without disclosing the interest rate risk in its portfolio. Many retirees and retail investors without sophisticated knowledge of financial markets and products can be easily fooled by SWAN’s marketing materials and invest in the SWAN ETF without a proper understanding of the duration risk embedded in the product.

Risk To Cautious View

The biggest risk to my cautious view is if the economic data turns negative and a recession occurs, then the negative correlation between stocks and bonds may reassert itself and the SWAN ETF will perform as expected in that situation. However, as long as we are in the current environment of strong economic growth and simmering inflation, the Fed may continue to hold interest rates ‘higher for longer’ and cause duration losses to long-term treasury bonds.

Conclusion

The SWAN ETF claims to use stock options and ‘safe’ treasury bonds to engineer a product that delivers participation in S&P 500 returns while protecting against drawdowns. Unfortunately, the SWAN ETF has been failing in its mandate, as equity drawdowns in the past 2 years have been mostly driven by rising interest rates, which have caused large losses to SWAN’s portfolio of treasury bonds.

I recommend investors avoid overly financially engineered products like the SWAN ETF unless they understand exactly the risks they are taking, as there could be undisclosed risks involved in seemingly ‘safe’ investments.

Read the full article here